We review the March 19 2015 Oliver Wyman and Morgan Stanley report, “Wholesale & Investment Banking Outlook.” This report got a substantial amount of press – we wanted to see if it lived up to the hype. Our conclusions are that OW and MS discuss the current reality well and there isn’t that much new to advertise. The interesting parts are speculative and include a fair amount of consultant and analyst guesswork. We rate the realism of the estimates.

The report is subtitled “Liquidity Conundrum: Shifting risks, and what it means.” In truth, most market participants know this stuff already. Fixed income liquidity is shrinking and no amount of electronic trading will help. The old market was built on market makers and banks buying and selling their own inventory. Basel III and its local variants have made this unprofitable, plus buy and hold players (Central Banks, banks needing High Quality Liquid Assets) are eating up supply making the remainder that much more illiquid for trading.

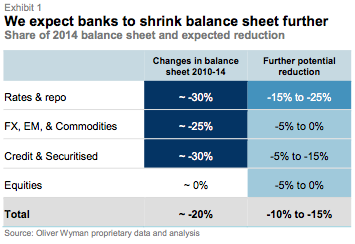

The first punt of the report comes early, on page 3:

That’s a pretty dire prediction for rates and repo. On a bilateral basis we agree with the further potential reduction, and even would suggest that the figures would go lower. However, enter the CCP: centrally cleared trades could stem the decline and may even reverse the course if the economics are there. We note that OW/MS is focusing only on the “largest wholesale banks.” We are already seeing smaller banks and non-bank actors step into this space. It is possible that the big banks decline by another 15% to 25% in their rates and repo business, but that does not mean a decline by that figure for the industry as a whole. (Keep an eye on TrueEx, DTCC, CME, etc.)

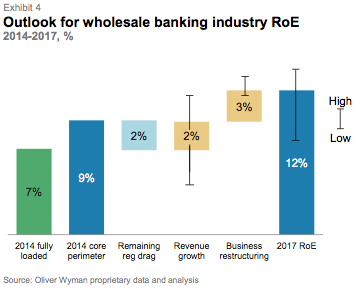

The next guesstimate looks at what change still needs to happen to get to a 12% Return on Equity figure. This is equivalent to saying that banks can get 2% growth organically but will need to dig deep in restructuring in order to make a 10% return. That’s the 2% in “remaining regulatory drag” and 3% in “business restructuring.” Is this right? Who knows, but its a great sound bite.

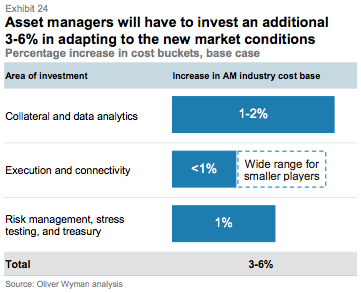

OW and MS argue that asset managers have a greater spend ahead of them to get ready for new regulations, and that collateral and data analytics will add 1-2% on today’s total industry spend. While perhaps true for the industry, this spend will be highly skewed towards the large firms that are engaged in collateralized trading activities. A plain vanilla long only manager barely needs to bother with collateral today let alone tomorrow. We have found repeatedly that “the buy-side” is highly diverse. That should be remembered when hearing generalized statements about demand. We’d like to see the segmentation of what portion of the market OW and MS think will be impacted vs. what won’t be at all.

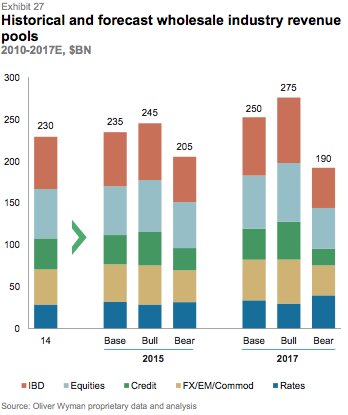

We have no argument with the following chart – its just sort of fun to think about. The base estimate really isn’t bad. Its that bear estimate that will have CEOs worrying (and management consultants employed).

And finally:

“There is also value to be captured on the back of increased disclosure and transparency for the industry, particularly for those who manage to link static data with flow data. One specific example is collateral optimisation, which will become ever more critical as end-user collateral demands continue to increase. At this stage, incremental revenue pools are difficult to size. Based on current data spend, and client willingness to spend on more effective data / asset / risk management solutions, we could see a revenue pool of $0.5-1 billion emerge over the next 3-5 years. However, this will be split across a broad range of market infrastructures and banking intermediaries, as well as banks.”

Come on, this one is just made up. The spend on collateral optimization will be directly correlated to how much savings this produces internally for each firm. That in turn will be driven by collateral shortages, bottlenecks, the work of infrastructure providers and others. Its another great sound bite, and one soundly bitten by Global Custodian among others, but this doesn’t sound like a logical conclusion to us.

The press release for this report is online here.