The Treasury Market Practices Group (TMPG) released a consultative white paper on clearing and settlement in the market for US Treasury secured financing transactions (SFTs), which include both repurchase agreements and securities lending agreements. The white paper describes the various clearing and settlement arrangements for US Treasury SFTs, provides detailed maps that illustrate the process flows, and catalogs potential areas of risk.

The TMPG seeks public feedback on the following aspects of the secondary Treasury market:

- the accuracy and completeness of various SFT clearing and settlement arrangements described,

- risk and resiliency issues identified, and

- any other feedback and suggestions.

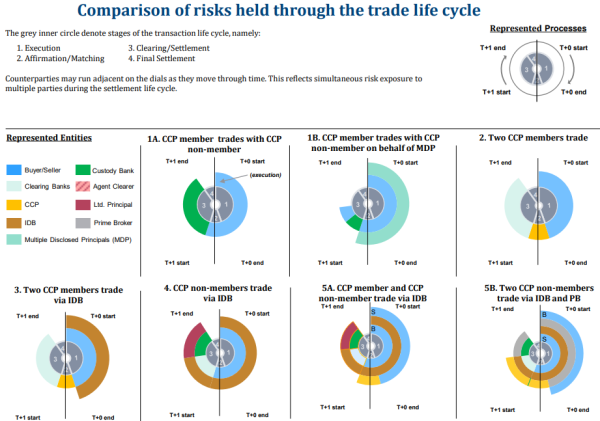

The Treasury market has seen significant changes over the last two decades, including the increased use of advanced technology by execution venues, widespread use of automated trading strategies, and the emergence of new types of market participants. Clearing and settlement are typically benign post-trade processes, but they may be disrupted by contingent events that could create or exacerbate market stress.

Given these concerns, the TMPG committed to study clearing and settlement practices for US Treasury securities. The white paper builds on the TMPG’s previous finding that market participants may not be applying the same risk management rigor to the clearing and settlement of their cash US Treasury activities as they do in other aspects of risk taking.

Specifically, the Group’s new consultative whitepaper notes that, overall, clearing and settlement for SFTs is fragmented, third-party credit extension arrangements may not be fully understood, and the opaqueness of the SFT market may obscure some participants’ ability to accurately identify and manage clearing and settlement risks. For non-centrally cleared bilateral SFTs, clearing and settlement is bespoke and opaque. For non-centrally cleared bilateral SFTs and agent-cleared tri-party repo, positions carry counterparty and liquidity risks, with potential systemic implications during times of stress.

“The US Treasury securities market is the largest and most liquid sovereign bond market in the world. It is important that we as market participants appropriately manage risks associated with transacting in this market under a wide variety of economic scenarios. The white paper outlines key risks to consider and I encourage all market stakeholders to carefully review it and provide their feedback and suggestions to the TMPG,” said Gerald Pucci, chair of the TMPG, in a statement.