The US Federal deficit has been an absent topic in recent Presidential debates and skirmishes. Certainly it is less enticing to the general populace than the latest scandals and accusations. However, recent high volatility and cost spikes in government liquidity markets show that this important policy topic should remain in the spotlight for regulators and banks.

In almost every Federal election in recent memory – at least since the Roosevelt era – US government debt has been one of the key talking points. Whichever party is not in control of government purse strings is generally loudly critical of the incumbents’ fiscal irresponsibility, while those in power find it necessary to justify themselves or deflect the issue. At least to date, neither the Trump nor the Clinton camp have had much to say on the US deficit. When discussed at all, it has been merely used as a peripheral example to illustrate the larger point of the other’s questionable competency – not as a pivotal concern in and of itself. Indeed, apart from some of the most traditional Conservatives and Libertarians, the size of the federal debt has become an accepted fact of life. From a political perspective, the question has become far more about how the debt continues to grow – what spending habits/tax breaks are socially and politically justifiable – rather than whether the debt should be reduced as a goal in and of itself.

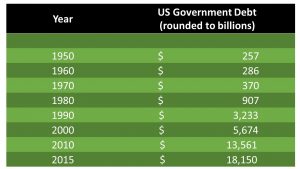

For context, let’s look at the federal deficit by decade since 1950. (Exhibit 1).

Source: www.treasurydirect.gov

We want to focus attention specifically on the post-Crisis, post Basel-II and III, post Dodd-Frank period of 2010 to present. As generally estimated, the government repo market stands at approximately $10 trillion outstanding globally at any given time, the largest percentage of which is in US government instruments. A likely figure of the percentage of outstanding US government debt that is “in play” – that is, consistently available for the markets’ liquidity needs – may be about 35 to 40 percent. The rest is tied up in central bank currency reserves, corporate coffers, and other holders that are not generally considered reliable liquidity providers.

That does not appear to be enough to meet the needs of the market, particularly in times of even mild stress. As we reported earlier this year, the mini-crisis that failed to materialize around Brexit caused a massive spike in repo rates for a day or two. This quarter end, when SEC rules around brokerage money market funds came into full effect, we saw another and perhaps more lasting inversion in the governments market. What is concerning, of course, is that neither of these events really has approached a true economic and/or market shock – such as might occur during a US-China trade war, for instance; or the implementation of the NSFR capital standard or the collapse of a G-SIB. In these events, liquidity will further contract to not 35 to 40 percent of debt outstanding, but perhaps 20 to 25 percent (or less)… assuming no particular emergency intervention on the part the Fed or other central banks.

Markets are now thoroughly addicted to US Treasuries as one of the only ways to remain compliant with current capital standards. This is a real and present danger, and one that has been created for the markets by regulators based on a profound shift in assumptions unthinkable as lately as a decade ago – the assumption that the US Federal deficit cannot ever be reduced. The concern regulators should have is that the US electorate or an effective political leadership takes a real interest in challenging that assumption.