The US Treasury end of year repo market exhibited only a short spike in rates that quickly quieted down. Under the surface however, variations in tenors and issue runs showed volatility that should be noted by both market participants and regulators. Left unattended, these variations could turn into a greater market concern at the next point of balance sheet constriction.

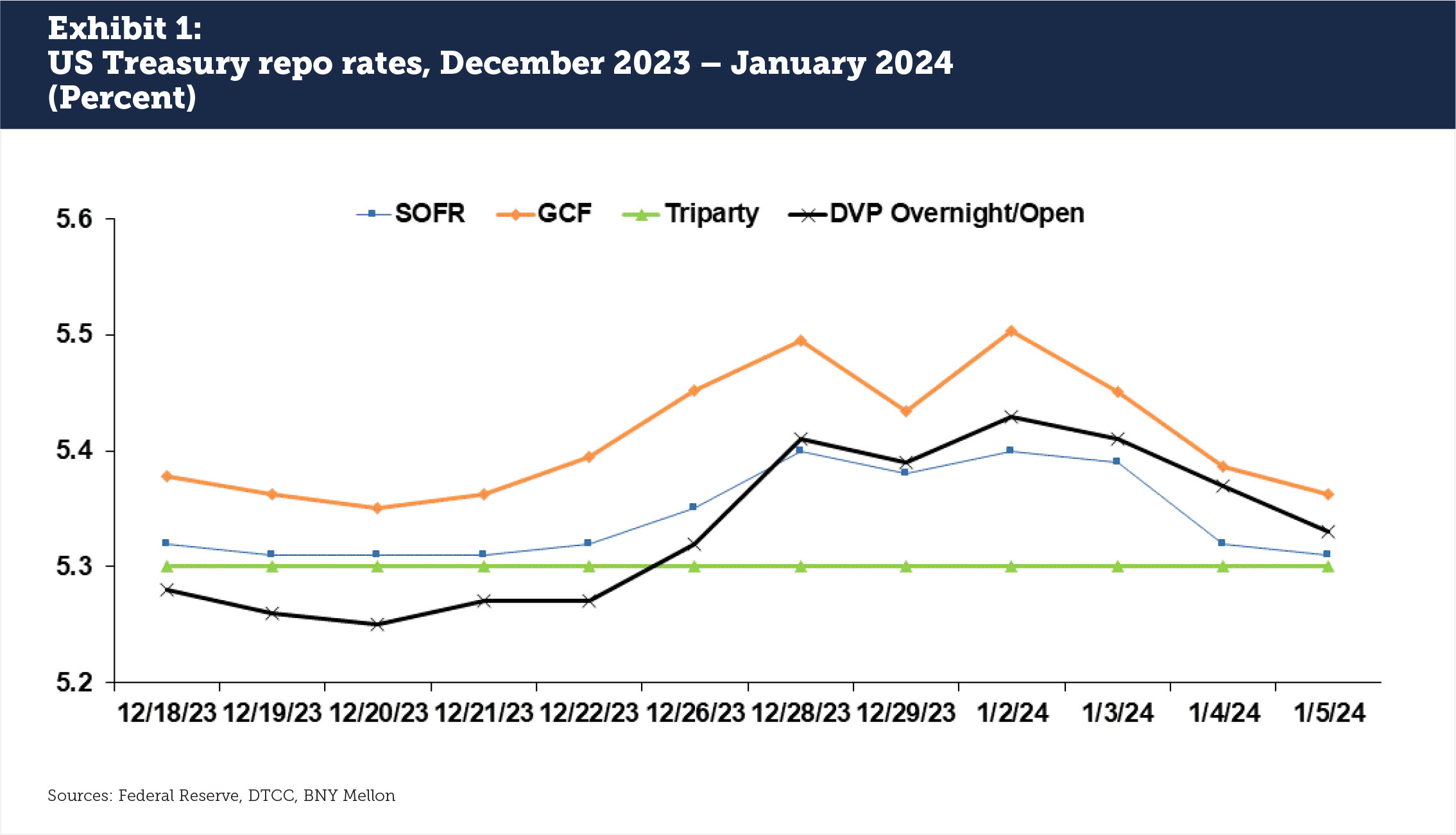

The high level picture of US Treasury repo rates showed an expected run-up through the last week of December 2023 followed by a quick decline. Across GCF® Repo, DVP Overnight/Open transactions and the Secured Overnight Financing Rate (SOFR), rates gravitated upwards by a basis point or two from triparty and the Fed’s Reverse Repo Facility (RRP) (see Exhibit 1). Compared to the outsized spikes seen in US Treasury repo on other occasions, most notably September 2019, the big picture on US Treasury rates suggests that the end of 2023 was uneventful.

As bank balance sheets shut down for the year, a need for liquidity drove money funds to the Fed’s RRP in a way that was unsurprising, but that generated some concern in the popular press. Reuters noted that SOFR hit its highest point since the rate was published in 2018. The rise in SOFR to 5.4%, from 5.3%, reflecting the movement away from RRP to private sector business, is more business-as-usual than a SOFR that sticks at one rate due to large volumes in the RRP. Some SOFR volatility could and should be expected.

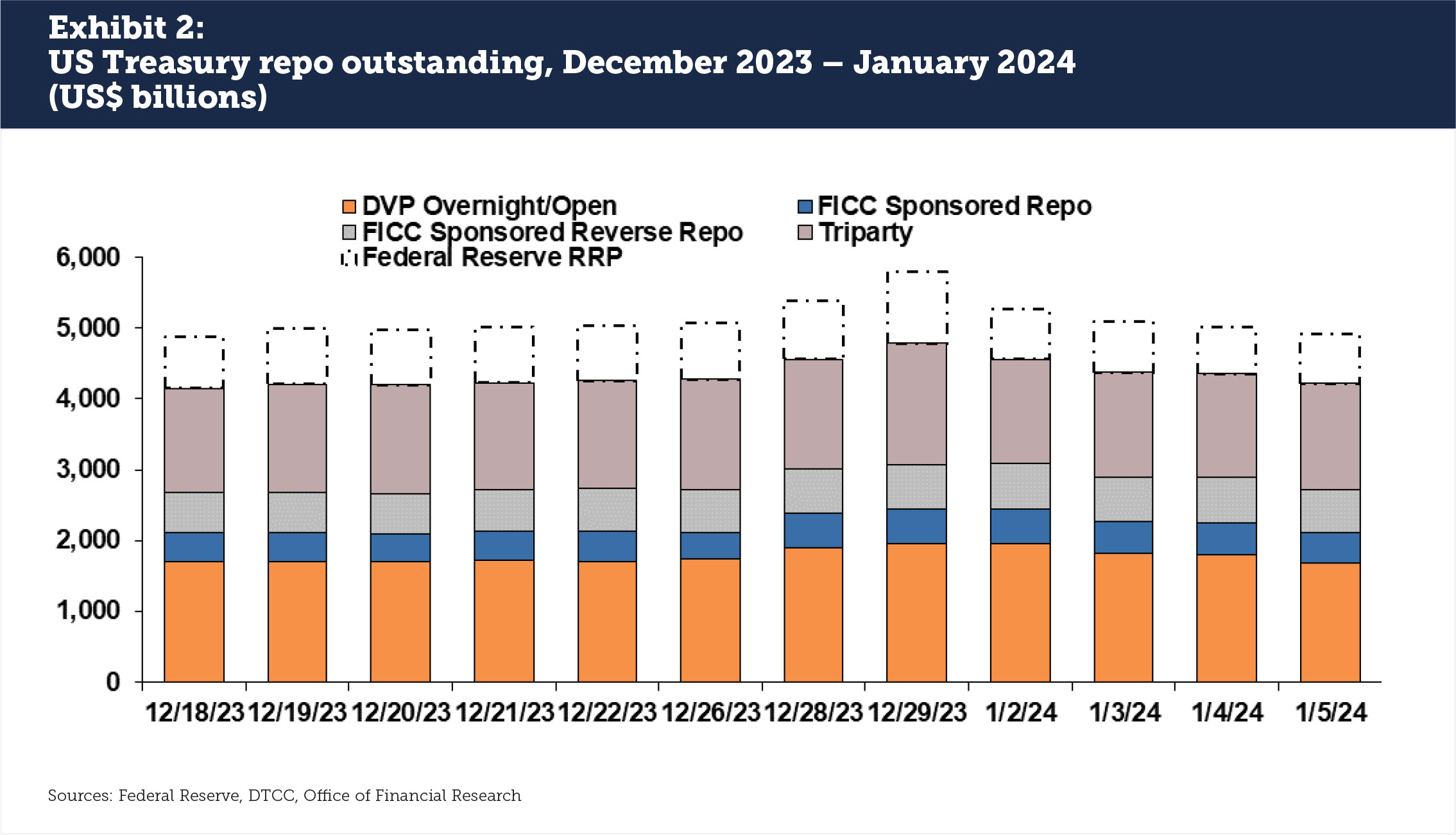

Volumes were also largely in line with expectations. On December 29, 2023, a total of $4.8 trillion showed what could be considered the limit of private sector market capacity at year end, with DVP and FICC’s Sponsored Repo business seeing the greatest upticks (see Exhibit 2). There was no Standing Repo Facility business at all through year end, indicating a lack of market stress at dealers.

Meanwhile, RRP business increased from its mid-December range of $700-800 billion to over $1 trillion before falling below $700 billion again by the end of the first week of January and below $600 billion by mid-January. Appropriately, the RRP picked up the slack as repo dealers hit capacity. We do not see an increase of $300 billion in RRP business at the end of the year as much to be concerned about, especially as money funds reduced their RRP usage from a high of $2.4 trillion in April 2023.

There has also been some thinking that further declines in RRP balances could encourage the Federal Reserve to slow down Quantitative Tightening, a move that would be beneficial for the broader economy. Speaking at a panel on Market Monitoring and the Implementation of Monetary Policy in early 2024, Dallas Fed President Lorie Logan said that “given the rapid decline of the ON RRP, I think it’s appropriate to consider the parameters that will guide a decision to slow the runoff of our assets. In my view, we should slow the pace of runoff as ON RRP balances approach a low level.” The year-end 2023 increase followed by another sharp decline may be seen as a step in the right direction for Logan’s argument. Speakers at Finadium’s Rates & Repo US conference in November 2023 agreed that the RRP is an important metric to watch as relates to QT decision making.

Volatility in the Details

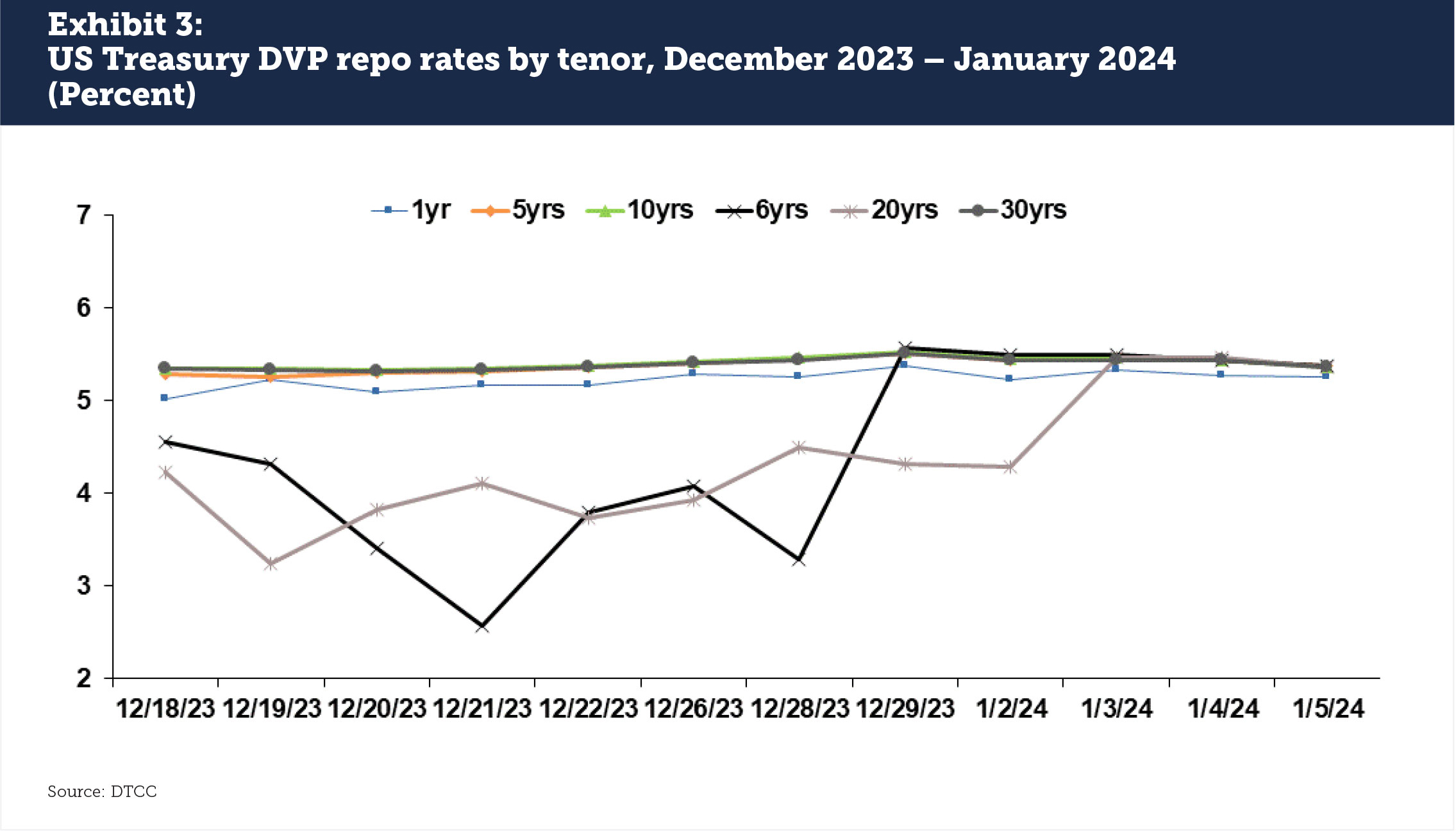

Not all US Treasury issues traded with the same stability however, a fact that should be considered by both market practitioners and regulators. Data from DTCC’s Treasury Kinetics service showed that 20 year and 6 year bonds traded special, with 20 years bouncing back to average rates for other tenors right at the end of the year and 6 years returning only a few days after the turn (see Exhibit 3). Traders told Finadium that demand for the 20 year has been consistent through the hiking cycle, and that street demand increased as the Fed did not lend out any 20 years through the SOMA account.

DTCC Treasury Kinetics data show that 20 years had been alternating between specials and General Collateral on multiple occasions through H2 2023, with a low rate of 3.24% on December 19 following another hard to borrow run in September. The 6 year on the other hand turned special only in December 2023 with a low rate of 2.57% on December 21.

20 year and 6 year bonds represented a small part of the overall DVP market, with 20 years at 3% of total volume and 6 years at 1%. The big volume collectively was in the 5, 7 and 10 year bonds, which comprised 61% of DVP activity. However, the variation in rates by tenor shows that it would be unwise to assume that the average rate published for all securities means that was also the average for each individual tenor. Outsized special interest in the 10 year, for example, could have moved the DVP average by a percentage point downward at a critical time with implications for dealer desks and SOFR averages.

On the Run/Off the Run

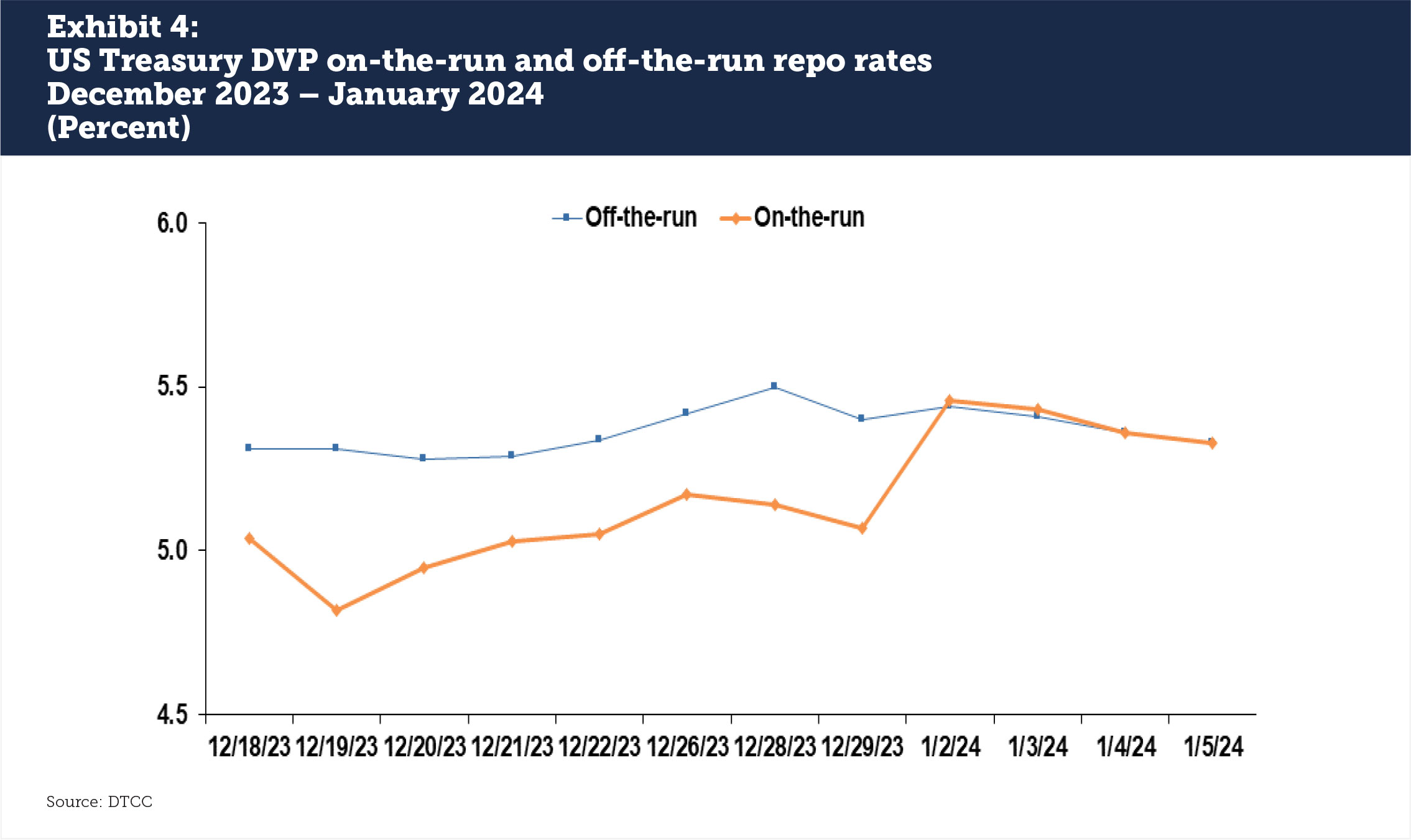

Another point of variation in US Treasury repo rates at the end of the year was between on-the-run and off-the-run securities. DTCC DVP data show that 85% of US Treasury repo business at the turn was in off-the-run issues, which had repo rates as high as 49 basis points over on-the-run issues in the last weeks of the year (see Exhibit 4). This suggests a structural pricing imbalance in financing made more acute by the large amount of recent US Treasury issuance across all tenors.

It does not appear that easing financing rates is on the agenda of the US Treasury in their buyback plans: according to the US Treasury’s Assistant Secretary for Financial Markets Josh Frost in a September 2023 speech:

We believe buybacks can help improve the liquidity of the Treasury market by providing a regular opportunity for market participants to sell back to Treasury off-the-run securities across the yield curve. This should improve the willingness of investors and intermediaries to trade and provide liquidity in these securities, all else equal, knowing there is a potential outlet to sell some of their off-the-run holdings.

The spread between on-the-run and off-the-run financing rates supports the idea that the US Treasury would buy back older issues, but that may not be the case. According to Anthony Tarabocchia, Head of US Repo at MUFG Securities Americas, “less supply would naturally create more demand to borrow. I think any buyback approach should be slow and steady to not disrupt the current demand/supply dynamic in off the run Treasuries.” While the size and scale of the buyback program remains to be seen through 2024, a greater ability for off-the-run Treasury holders to sell as needed could result in less need to finance, hence easing demand. Conversely, more issuance and greater end of year financing needs could put more pressure on end of year repo rates, leading to greater spikes as a result of simply more US Treasury issuance outstanding.

This article was commissioned by DTCC Data Services. For more information, please visit https://communications.dtcc.com/dtcc-treasury-kinetics-contact-us-LP9155A1LA1.html.

The observations and outlook expressed reflect solely the opinions of Finadium and the author.