With all the noise about SFTR, it’s often hard to separate out what is useful vs. what is just more agitation. The new white paper from DTCC and the Field Effect, “Addressing SFTR’S Industry Impacts: The Vital Role of Trade Repositories,” has some valid points for both newcomers as well as industry insiders. Take a hard look at the figure citing a 5X reporting volume increase.

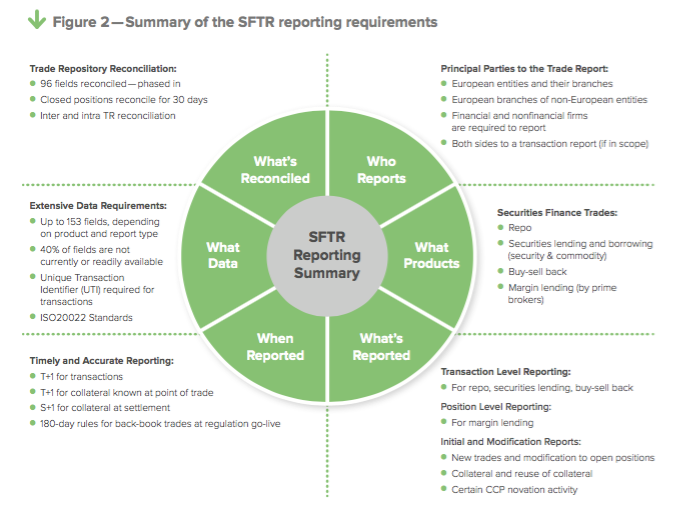

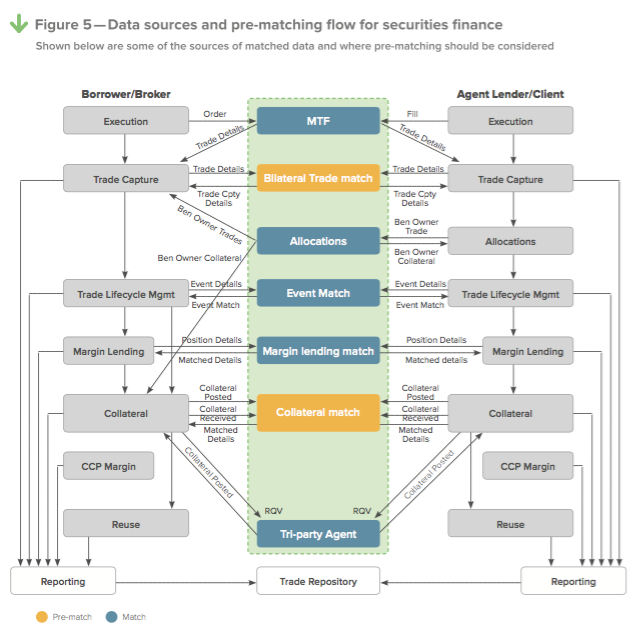

The paper provides a helpful summary of what SFTR is. This information has been published elsewhere but some nice visuals deliver the story. The majority of the paper is good reading for lawyers, senior managers and others with less direct experience who need the overview. For instance, if you want to show your boss’s boss what actually needs to happen, then print out the Figure 2 and post it by the coffee maker. Do not show them Figure 5, which, while entirely accurate, can cause blurred vision for newcomers. If you know by heart that SFTR has 153 fields, then most of this paper is not for you.

Source: The Field Effect (C)

Industry professionals should check out the sections on disclosures by agent lenders and brokers and on trading over MTFs. While all of these ideas have been around for a while, the paper provides some useful examples of how reporting requirements will create industry change:

- SFTR will make ALD obsolete: “If the agent lender uses the current agent lending disclosure (ALD) process to disclose the beneficiary to the trades post settlement, the borrower will not be able to meet its SFTR reporting obligation on time. In addition, beneficiaries will need transaction-level (including intraday trades) and collateral information from their agents in order to meet their SFTR reporting obligations.”

- Prime brokers have big unanswered questions on margin reporting: “For an ML position between a PB and its hedge fund client, the position held by the hedge fund will be deemed as collateral covering that loan, however large or small. But it’s unclear whether this is just what will be deemed as margin in the PB’s margin calculation or everything held in all accounts covered by a European PB agreement at the LEI level of the hedge fund. As a result, the hedge fund’s positions may need to be reported to the TR regardless of the size of the ML and, as the PB would be in scope, regardless of the jurisdiction of the HF manager.”

- Electronic trading venues will gain traction: “For transaction reporting, firms should leverage MTFs for UTI generation/sharing and increasing the level of matched data included in the reporting function. Firms should look at their bilateral business activity and assess where they can move it to MTFs and increase straight- through or zero-touch processes across trade ow and client segments.”

How about the claim that SFTR will result in a 4X to 5X multiple of reporting obligations relative to trading volumes? Calling it 4X or 5X is a big punt, but we agree that the level of reporting for each repricing, collateral change, close out, rebooking, etc. will be big, regardless of whether this is the beginning of end of a trade. As the report notes, “in securities lending a mark will result in a modification report and a valuation report, and intraday bookings must be included — across the whole book.” The actual multiple could wind up being 10X. But since DTCC is behind this paper, the 5X number is likely to stick, much like the quote from years ago that margin call activity would increase by 1000%. Was it right? Who knows, but the citation has been repeated countless times.

All in all, a good overview from the Field Effect. The full paper is available at www.dtcc.com/addressing-sftr-industry-impacts