Synthetic prime brokerage has become an important part of hedge fund financing and relationship management. While choosing a synthetic vs. cash transaction in the short-term may be dictated by the ease of set up, there are longer-term implications that funds should consider when structuring their prime brokerage agreements. This article looks at the pros and cons of synthetic vs. cash financing for hedge funds. A guest post from Scotiabank.

Across trading, financing, initial public offerings (IPOs), access to research and other services, cash prime brokerage is the mainstay of the business. Large and small firms offer it, and it is a principal way for hedge funds to show their stability to investors. Every fund in the US$4.5 trillion hedge fund industry has one or more cash prime brokerage relationships (source: Barclayhedge).

Alternatively, a synthetic trade produces the economic equivalent of a cash investment without the actual purchase or sale of securities. This makes synthetic ideal for trading in markets where international participation may be limited or there are high trading or settlement transaction costs. Total Return Swaps (TRS) are the best-known product in the synthetic market thanks to Archegos, but various forms of over-the-counter (OTC) derivatives serve similar purposes with names like Portfolio Swaps and Contracts for Differences. The objective remains the same: investment exposure minus the holding of underlying securities positions.

In financing, revenues generated from synthetic transactions have held steady over the last few years, compared to the cash market that has seen greater amounts of margin leverage and lower amounts of net revenues. A combination of banks’ internal resource optimization, meme stock disruptions and regulations are the source of change. In H1 2020, synthetic prime brokerage represented 54% of prime brokerage financing revenues, compared to 46% for cash margin and short-sale financing revenue.

Both the cash and synthetic prime brokerage markets offer advantages and disadvantages to investors. Hedge funds should be aware of what these differences mean for their trading and relationship management activities, and how upcoming regulatory changes, discussed later on in the article, may adjust their decision parameters.

The pros and cons

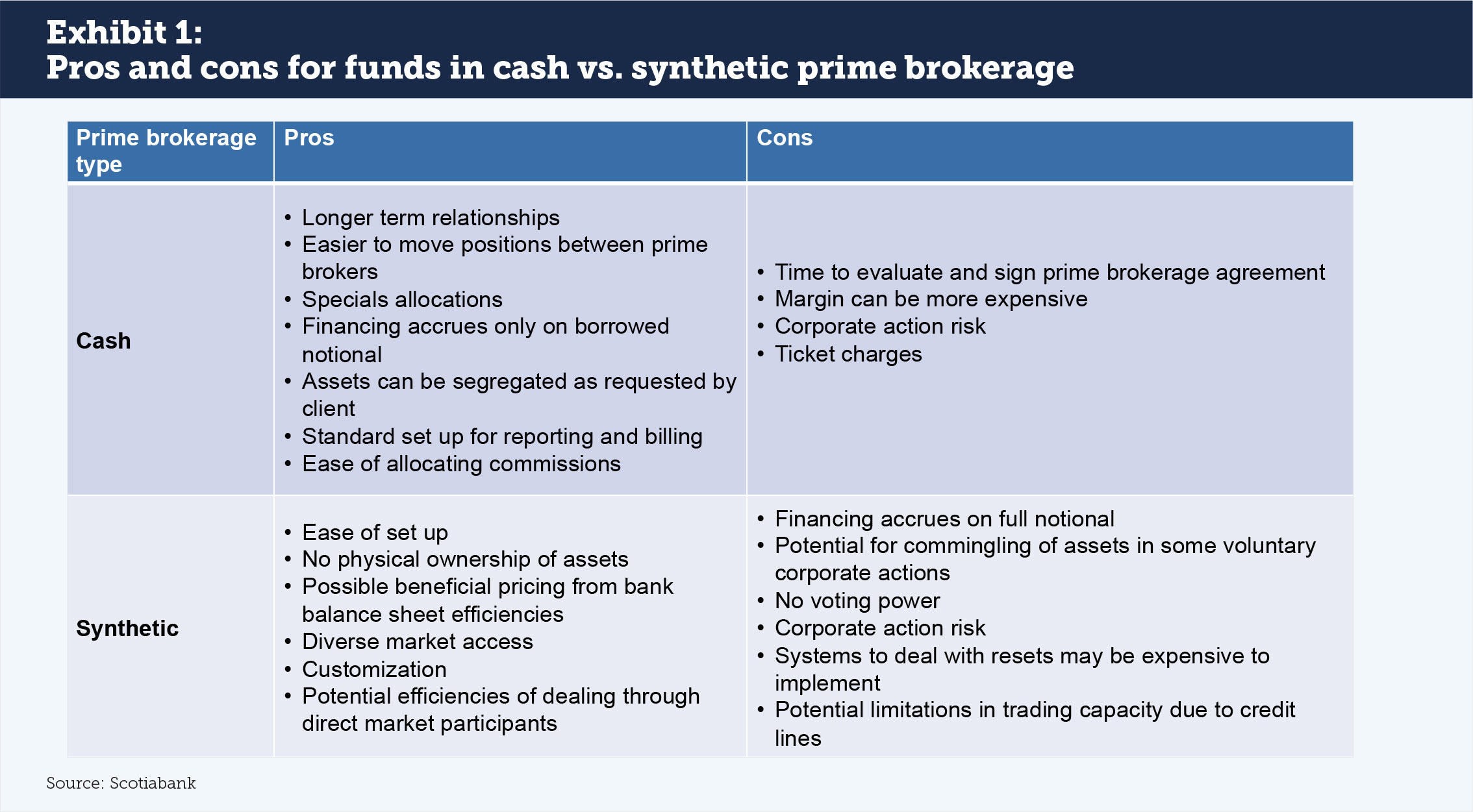

There are a range of opportunities and challenges to consider when selecting a synthetic or cash prime brokerage relationship (see Exhibit 1). Synthetic prime brokerage has been beneficial for bank capital ratios; Basel III rules can encourage banks to trade synthetically due to lower Leverage Ratio requirements compared to physical-leveraged transactions. The impact of OTC derivatives is less on the Leverage Ratio and more on the Liquidity Coverage Ratio, which tends to be a less binding constraint.

For hedge funds, synthetic offers an easier set up than physical prime brokerage using International Swaps and Derivatives Association (ISDA) agreements as the industry standard. As there is no custody of assets in a synthetic relationship, swaps can be customized to meet investor needs and fund positions can be kept anonymous (pending regulatory changes), as any hedges are held in the name of the prime broker. There are also opportunities to take advantage of street-wide balance sheet requirements to obtain financing rates. For example, if a bank needs to be long or short to match up their book, funds can take the other side at a lower cost than the same trade in the cash market. While it cannot be taken for granted that such trades will happen, they can provide pricing benefits when they do.

There are advantages to cash prime brokerage as well. Relationships between hedge funds and prime brokers tend to be longer term than for synthetic-only trading arrangements. This often leads to better information flow and a potential prime broker willingness to extend margin, since more is known about the client’s activities. It is also easier for funds to move positions between prime brokers as there is no lock-in to a swap position with a counterparty, and there are existing standards for reporting and billing that all prime brokers recognize. This makes comparing costs between prime brokers easier than for synthetic prime brokerage.

How margin is managed across synthetic and cash positions may drive hedge funds to choose one structure over the other. At some primes, margin is not dynamic in a synthetic position – a primary reason for the Archegos failure was an inability to manage swap margining rules. Financing costs accrue on the full value of the notional position in synthetic, which may make a good rate less interesting than the total charge. In cash prime brokerage, margin locks may be more flexible and financing costs accrue only on what is borrowed, although margin rates may be more expensive at first glance compared to the synthetic alternative.

There may also be regional differences for why synthetic versus cash makes more sense. European markets tend to be more swap-driven, partly in response to stamp taxes and the nuances of physical ownership of securities in different countries. This began with the growth of the Contracts for Differences market and has continued, with banks and their clients internalizing efficiencies in swaps transactions. By contrast, trading interest in the US market tends to be more standardized around cost and ease of set up.

Making the right decision for the fund and the trade

Synthetic versus cash prime brokerage is not an all or nothing proposition. It may be appropriate for funds to have both types of relationships, including trading cash and synthetic products with the same prime broker counterparty. At the same time, there is value in deciding whether synthetic or cash should be preferred, and why.

Funds should also be aware that some of their decision factors may change in 2022. Position anonymity from TRS trading may be valued now, however, proposed rules from the US Financial Industry Regulatory Authority (FINRA) on short-sale transparency, a US Securities and Exchange Commission proposal on TRS reporting, a draft bill from the US House of Representatives on 13F reporting, and a review of the Short Selling Regulation by the European Securities and Markets Authority, may result in less firm-level transparency than hedge funds have been used to seeing. On the bank side, the implementation of Basel III’s Net Stable Funding Ratio (NSFR) is making swap costs more punitive, which could lead to material pricing changes. Both of these factors may result in a renewed preference for cash prime brokerage.

While these options may be complex, the takeaway is to decide how your fund wants to approach its relationships. Is the prime broker meant to be a short-term or long-term trading counterparty? Will a stronger overall relationship translate into better access and financing terms? How do voting rights or corporate actions impact fund operations or objectives? These are key questions to consider when deciding what’s better for your firm, a cash or synthetic prime brokerage.

About the Author

Brendan Eccles

Brendan Eccles

Global Head of Securities Lending

Scotiabank

Brendan has been a member of the Scotiabank Prime Services team since 2004. He began his career at Scotiabank in Toronto as a trader on the Securities Lending desk. In 2006, he moved to New York to launch the US Securities Lending product. In 2013, he was promoted to North American Head of Securities Lending and in 2015 was promoted to Global Co-head of Securities Lending. Prior to joining Scotiabank, Brendan worked at another Canadian financial institution as a Securities Lending Trader from 2002 to 2004. Brendan holds an Honours Bachelor of Science, Science & Business (Chemistry Option) from the University of Waterloo and is a CFA Charterholder.