Securities lending indemnification for investor portfolios continues to be heavily in demand. However, regulations and the ensuing capital charges associated with providing indemnification are increasingly changing how indemnification is perceived, offered and priced. A guest post from BNP Paribas.

Many agents offer their participants varying levels of indemnification options for their lending and collateral reinvestment programs. Indemnification is an important part of the agent lending business and is a key consideration for many investors engaged in securities lending. Investors should be cognizant of how their programs are evolving and the options they have in today’s regulatory environment.

What is indemnification?

Indemnification is an insurance policy that protects investors against borrower credit risk. Indemnification means that, in the event of a counterparty default, the agent would first use the available collateral (typically collateralized from 102-105%) to repurchase the client’s securities or return an equivalent amount of cash to their account. If the collateral were insufficient to make the investor whole, then the agent lender would use its own capital to repurchase the client’s securities or return an equivalent amount of cash to their account. Indemnification can also be applied to the reinvestment of cash collateral. The cash collateral reinvestment in a client’s securities lending transaction may also be indemnified, but this is not as universally common as indemnification against borrower counterparty default risk.

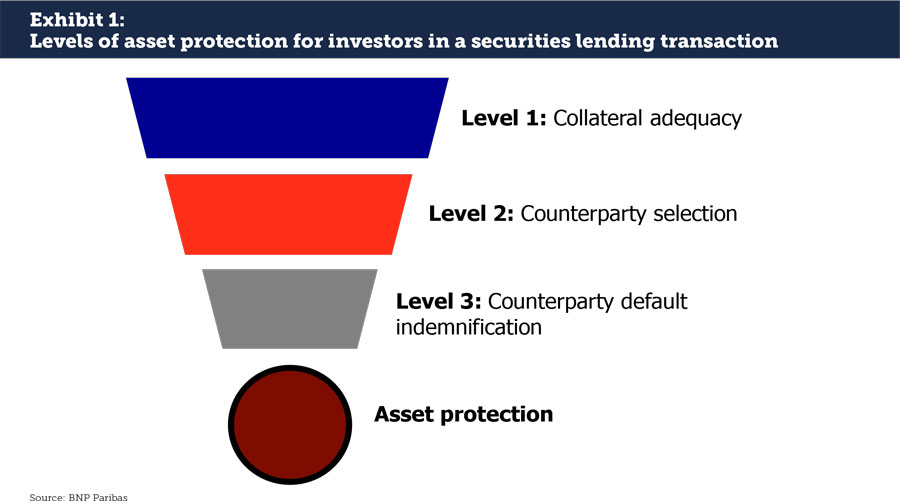

Even with indemnification, a careful selection of borrowers and adequate collateral are the most important risk management practices for an agent lender and its investor clients (see Exhibit 1). Indemnification is the final layer of protection provided by an agent lender in the unlikely event that collateral selection and counterparty selection are inadequate protections. Therefore, it is imperative that the party providing the indemnification is well capitalized and possesses excess liquidity to meet the potential demands of indemnification in the event of a counterparty default. It is also equally important that the party providing the backstop to the transaction utilizes a diversified list of counterparties to minimize program exposure to any one borrower.

Indemnification remains important to investors

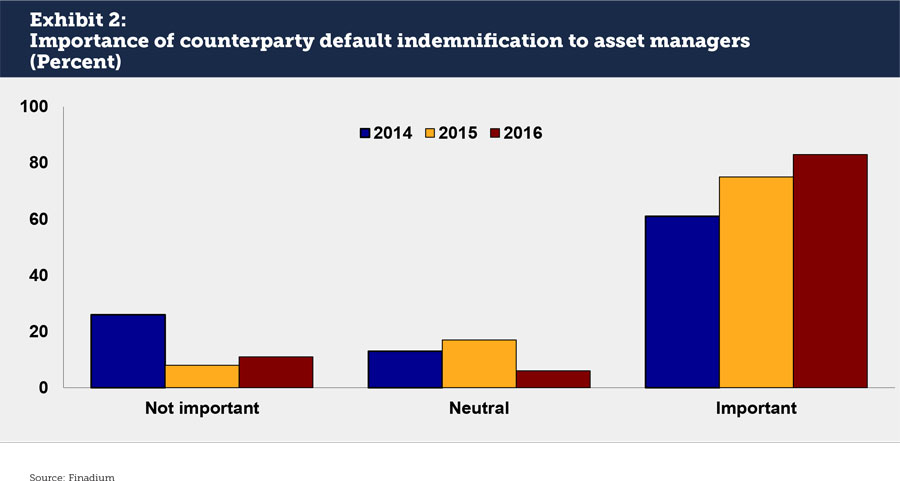

Indemnification in securities lending has been a standard industry practice for over 15 years, and has become a legal requirement or a near-necessity for many investors. Even those who are not legally obligated consider indemnification to be simply a good risk management practice. The perceived value of indemnification to investors has been increasing, even though there have been few uses of indemnification across the industry in recent years. Data from a 2016 Finadium survey showed that 83% of asset managers in North America and Europe thought that counterparty default indemnification was important for securities lending programs, up from 61% in 2014 (see Exhibit 2).

The costs to provide indemnification are increasing

While the importance of indemnification to investors has increased, the cost to agent lenders of providing it has increased far more. This is primarily due to Basel III and Dodd-Frank, which, together, seek to reduce risk in the financial system and increase the resilience of banks to potential market shocks. There are three major areas where regulation has increased the cost of indemnification:

- The Leverage Ratio. By offering indemnification and assuming some portion of the risk in a securities loan, the agent takes on an off-balance sheet liability that must be funded in order to keep the ratio at or above required minimums. The effect of this for the agent lender is that High Quality Liquid Assets must be reserved to support the securities loan.

- Counterparty exposure limits. Banks worldwide are limited to how exposed they can be to other banks. For example, a global agent lender may have a 15% total exposure limit to a prime broker borrower across all products. Indemnification would be one small part of the business, with FX, OTC derivatives and repo as potential candidates for other product relationships. The regulatory cost of indemnification and the profitability of securities lending must be considered across this product mix.

- Credit risk costs for collateral. Banks are required to assess a credit exposure cost to all collateral held in securities lending programs as part of the Basel Committee’s Standardized Approach to credit risk; this carries an outsized impact on non-cash collateral. While the rules are not yet finalized, it is expected that credit exposure capital costs for collateral will add some new price for indemnification. Without indemnification, an agent lender is simply moving assets for clients under the client’s own credit.

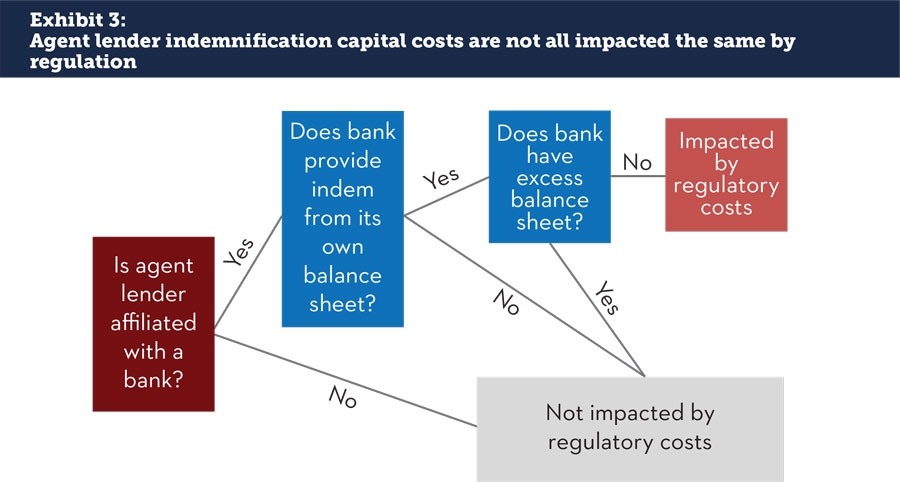

That being said, not all agent lenders are impacted by the cost of indemnification in the same way (see Exhibit 3). Much depends on the amount of excess balance sheet available for covering the Leverage Ratio liability that emerges from the cost of indemnification. For agent lenders that are divisions of banks, excess balance sheet means that the cost of indemnification is easily absorbed. Conversely, balance sheet limitations mean that providing indemnification may be expensive. There are also substantial variations across banks depending on jurisdiction, use of a Standardized vs. Advanced approach to capital calculations, and other regulatory differences.

Options for recovering the cost of indemnification

When agent lenders do not have balance sheet capacity, the cost of indemnification must be recovered by a combination of higher agent splits on lending fees and increased fees to borrower counterparties. Already, agent lenders in North America have been speaking with their clients about raising fees for indemnification or implementing alternative fee structures depending upon client preference.

Agent lenders have two other ways to recoup the costs of indemnification: increase fees for borrowers and reduce General Collateral (GC) loans. However, the success of this strategy is based on market conditions. In practice, one agent lender charging a higher rate for securities loans means reduced balances for their clients, which in turn reduces investor income through lending programs. Borrowers naturally seek the best rates available to them, and so will turn first to lending agents that absorb the indemnification costs internally.

Reducing GC loans means that agent lenders save their balance sheet capacity for the highest revenue-generating opportunities. GC loans have the lowest return but carry the same capital costs as Hard to Borrow or Specials transactions. Lower GC balances mean less cash for reinvesting in revenue-generating accounts, which in turn reduces the agent lender’s ability to lend securities across a variety of borrowers and in different market conditions. These factors combine to decrease revenues for investors.

Investors do not have to settle for increased fees or reduced revenues to order to receive counterparty default indemnification; the differences between banks and their regulatory requirements and balance sheet capabilities mean that pricing in securities lending fee splits is not the same across the industry. We have seen some significant pricing differences emerge between agent lenders for the same types of portfolios, all driven by indemnification. Investors in the securities lending market can profit by discussing the alternatives with a variety of agent lenders, especially as new regulations create new challenges and opportunities across different banking institutions.

Action Items for Investors

- Determine the value of indemnification to your organization: is it worth paying for?

- Consider if indemnification should be limited strictly to the loan transaction or extended to cover the collateral reinvestment?

- Determine how indemnification aligns the interests of your firm and your agent lender: if indemnification were not available for some or all trades, how would that change your risk profile?

- Price out indemnification in the market since agent lenders have different offerings – is this the time to issue a Request for Information (RFI)?

For more information on Indemnification and BNP Paribas:

Contact:

Lance Wargo

Head of Agency Lending

North America

+1 (212) 471 8041

lance.wargo@us.bnpparibas.com

Lance Wargo is North American Head of Agency Securities Lending for BNP Paribas. Lance has spent his  entire creer in agency securities lending. Prior to joining BNP Paribas, Lance held senior roles at E-Trade Securities and ClearLend Securities, a division of Wells Fargo Bank, NA. He began his career by supporting the lending desk, and performing numerous operational duties. He is an expert in areas such as settlements, cash flows, corporate actions, buy-ins, and in general, the operational foundation upon which securities lending is built.

entire creer in agency securities lending. Prior to joining BNP Paribas, Lance held senior roles at E-Trade Securities and ClearLend Securities, a division of Wells Fargo Bank, NA. He began his career by supporting the lending desk, and performing numerous operational duties. He is an expert in areas such as settlements, cash flows, corporate actions, buy-ins, and in general, the operational foundation upon which securities lending is built.