While the title of this article may sounds provocative, its actually a serious question. Recent Basel III rules on the Comprehensive Approach for securities lending credit risk analysis vs. the standardized approach for measuring counterparty credit risk (better known as SA-CCR) could realistically shift business away from securities finance transactions (SFTs) and towards OTC derivatives. Here’s why.

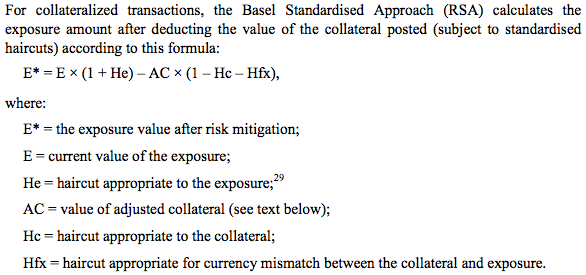

The collateral haircut/Comprehensive Approach measure arguably overstates credit risk to the banking industry. The problem is that the formula used for calculating credit risk is overly aggressive relative to existing VaR models, to OTC derivatives, and to the cost that financial intermediaries and their clients are willing to bear. Here’s the math (from “Strengthening Oversight and Regulation of Shadow Banking,” Financial Stability Board, October 14, 2014):

In the FSB’s version, the minimum capital requirement is then = 0.8 x RW x E*

This space doesn’t allow for running through all the numbers, but suffice to say, there is a very valid argument to make that the capital requirements of securities finance transactions get significantly raised relative to other options.

The damage doesn’t stop there. In the December 2014 “Revisions to the Standardised Approach for credit risk,” the Basel Committee proposed to take away an additional exemption it had left in for repo-style transactions. Although OTC derivatives were included here, the arrival of the SA-CCR in 2017 should take precedent:

“The current standardised approach includes exemptions to the 20% risk weight floor for certain repo-style and OTC derivative transactions. In particular, for transactions with ‘core market participants’, defined at the discretion of national supervisors, a 0% risk weight and a 0% haircut may apply under the simple and comprehensive approaches, respectively. The Committee seeks views on the implications and impact of eliminating this exemption (see Annex 1, paragraphs 95, 96 and 117).”

Meanwhile, the SA-CCR is clearly a benefit for the OTC derivatives market. We have proven this out for ourselves. A 2013 study by The Clearing House found that SA-CCR, formerly called the non-internal market model, or NIMM, “would be a clear improvement over CEM for measuring exposures on OTC derivatives due to its risk-sensitivity and granularity.” CEM refers to the Current Exposure Method, the model currently used by banks to determine OTC derivatives capital exposure. SA-CCR gets to use specific add-on calculations for each of five asset buckets, with models more closely customized to the risk of each asset class. The Comprehensive Approach for SFTs gets, um, nothing.

If we are in a situation that SFTs have a high capital charge but the same economic equivalent as an OTC derivative gets a lower capital charge, then where will the market go? To OTC derivatives. We already see this occurring in the growth of synthetic prime brokerage relative to physical (for more on this see the May 2015 Finadium research report, “Prime Brokerage: Towards a New Target Operating Model for Financing” Could a swaps structure be the norm for all SFTs going forward, with potentially a different collateral structure to reflect the need for cash financing, client expectations for a 100%+ collateralized securities lending transaction, or some mix? Sure, why not? The main obstacle may be clients who have not wanted anything to do with “derivatives” after 2008 but who are perfectly fine with securities lending and repo. But if the cost of a SFT is just too expensive, the market will find itself conducting OTC derivatives pretty quickly.