The Bank for International Settlements recently published its statistics on OTC derivatives trading activity as of end-December 2015. While the headline figure is an 11% decline in OTC activity from June 2015, this is misleading: the real shrinkage was caused by trade compression, not lack of interest or cost of doing business. Some other results were worth noting as well, especially in equity-linked derivatives.

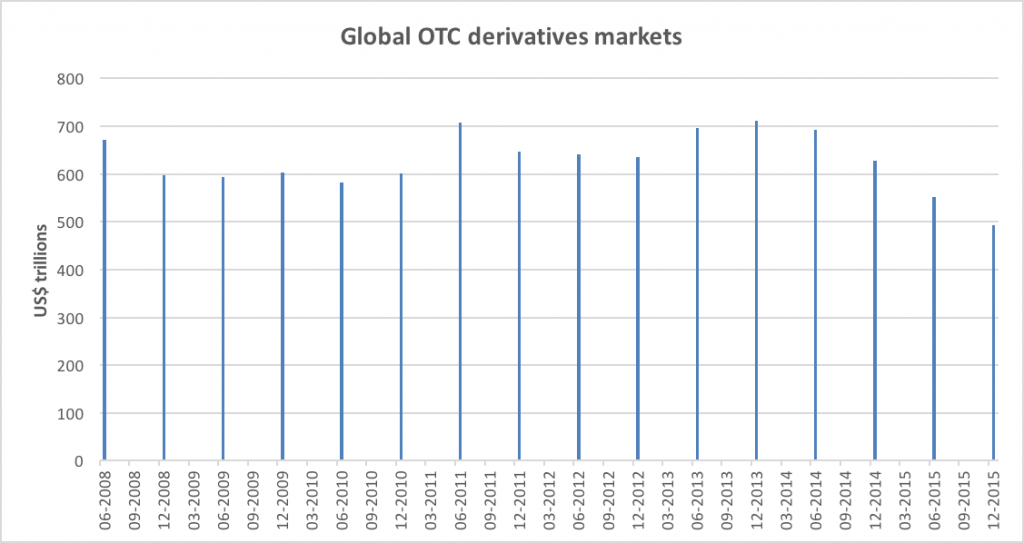

The notional amount of the OTC derivative market is now US$493 trillion. This is down very sharply from US$692 trillion in June 2014, a 29% decline (see chart below). Again, compression has driven the change.

The gross market value was US$14.5 trillion, on par with gross notional from 2007.

While the notional amounts of equity-linked OTC contracts fell slightly from US$7.5 trillion in June 2015 to US$7.1 trillion in December, we note that they actually are about flat from June 2014. Reflecting that the overall market fell by 29% over that period, the fact that equity OTC derivatives are flat is pretty significant. We see here the impact of physical financing costs, and our repeated findings that regulators have accidentally preferenced the OTC derivatives markets instead of the physical securities finance markets. Delta One desks continue to be busy.

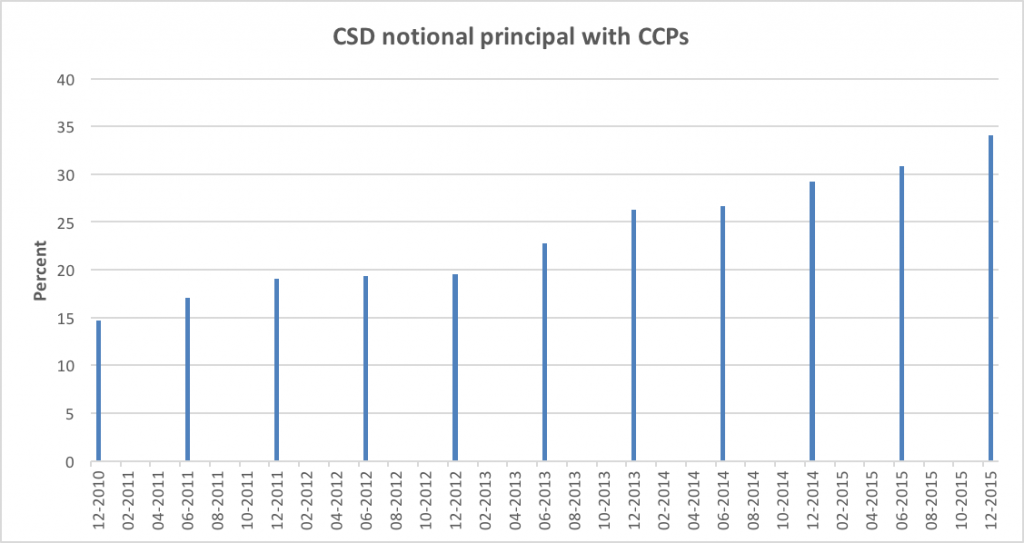

In Credit Default Swaps, the BIS notes the very sharp growth in central clearing, up from 10% in 2010 to 34% in December 2015 (see chart below).

Credit Default Swaps

For more on macro dynamics of the OTC derivatives markets using the BIS’s data, we recommend ISDA’s Cross-Border Fragmentation of Global Interest Rate Derivatives: Second Half 2015 Update. “The fracturing of the global interest rate swaps market that emerged in the aftermath of US swap execution facility (SEF) rules coming into force in October 2013 shows no signs of reversing. Although concerns over market fragmentation have been apparent for almost three years, some liquidity pools continue to be split on US and non-US lines.”

The BIS data are available here: http://www.bis.org/publ/otc_hy1605.htm

1 Comment. Leave new

Keep in mind that with that the ISDA fragmentation paper relies on SwapClear data that by LCH.Clearnet’s own admission can’t detect U.S. bank affiliates in the data. Hence, some of the “European” institutions may in fact be affiliates of U.S. banks, which could undermine the whole fragmentation story.

Keep in mind that with that the ISDA fragmentation paper relies on SwapClear data that by LCH.Clearnet’s own admission can’t detect U.S. bank affiliates in the data. Hence, some of the “European” institutions may in fact be affiliates of U.S. banks, which could undermine the whole fragmentation story.