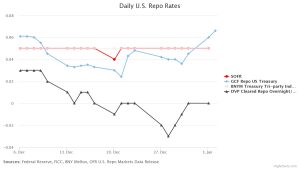

An argument for tight spreads in repo the last few years has been hyper low interest rates: if US triparty repo is 5 bps and GCF is 3 or 4 bps, then there is no room for dealers to charge 2 or 3 basis points in bid/ask spreads. But the Bank of England raised rates from 10 bps to 25 bps in December 2021 and thinking from the Fed is that inflation is not transitory after all (oops). US rates hikes of some sort are coming in 2022. Some parts of repo markets should benefit.

![]() This content requires a Finadium subscription. Articles with an unlocked symbol can be accessed with free registration. Log in or create a free account by signing up here..

This content requires a Finadium subscription. Articles with an unlocked symbol can be accessed with free registration. Log in or create a free account by signing up here..