The European Collateral Management System (ECMS) is a thoughtful way to harmonize what are currently 20 national central bank processes for collateral and credit management into one EU-wide system with the European Central Bank (ECB) at the center. In this article with Murex, we investigate how banks will need to consider their cash as collateral as a new ECB asset class, the risks and opportunities this offers, and what technology is required for the new framework.

The ECMS project has been ongoing for the last five years, building on the idea of European Capital Markets Union (CMU) to reduce competitive barriers and support the European financial sector. As part of CMU, European authorities have been working to create European-wide institutions and policies that replace a decentralized and costly range of infrastructures: these include processes run by national central banks, central securities depositories and central counterparties. The harmonization of operational and accounting practices is central to the mission of financial integration across the EU.

ECMS works by making the ECB the center of collateral transactions that occur with any of the zone’s 20 national central banks. This will make it easier for all the central banks to assess the credit and collateral position of their local counterparties and reduce the expense of supporting each central bank’s technology and process. ECMS will also harmonize the technology and functionality of TARGET2 and TARGET2-Securities, enabling one set of features for the three ECB liquidity, collateral and settlement services. Sabine Farhat, head of securities financing, lending and repo product at Murex, noted that “ECMS will support the European markets through its single view of securities and cash; this breaks down product and asset class siloes for the benefit of market participants.” CMS is built on the Single Collateral Rulebook for Europe (SCoRE), which creates standards for triparty collateral management, corporate actions and billing, using ISO 20022 messaging.

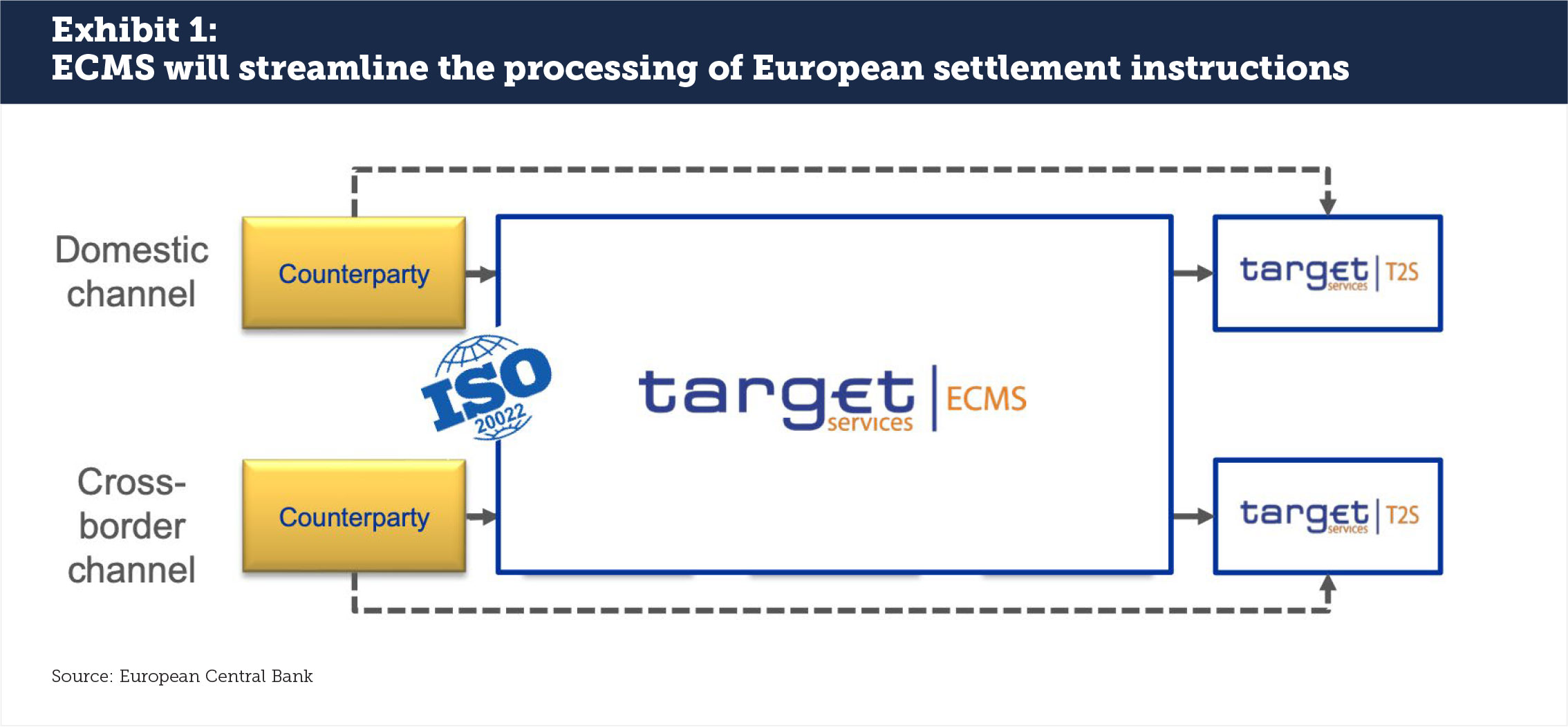

The aggregation of European collateral liquidity and settlement systems is expected to be operationally significant by reducing costs and creating one messaging format (see Exhibit 1). There are no economic studies that show the full impact across Europe yet, but the theory of reducing 20 different national central bank platforms down to one should theoretically assist financial markets by eliminating duplication. Similar to TARGET2 and TARGET2-Securities, there is also an element of competition in that the ECB will be operating services that private sector firms had previously delivered, albeit in a non-standardized way across the bloc. Our conversations suggest that the net result for Europe will be positive.

There is a new element of cash management that banks will need to solve for: while previous national central bank accounting looked at collateral and credit lines, ECMS will also look at cash as an asset class by calculating a credit line available to each bank counterparty. ECMS will have the ability to draw cash from a bank’s account as needed, which will drive efficiency but could also cause losses in interest revenue if not managed proactively. Similar to a margin account but with no need to request a distribution, the credit line becomes a new P&L input for banks using the ECMS service.

Cash as an ECMS asset

ECMS considers cash as one criterion in the available credit matrix for banking institutions. In a first instance, banks ask for specified credit lines, then ECMS calculates the daily credit available to each firm and sends information to a central liquidity management (CLM) database. CLM data is received from national central banks; this is a new function that consolidates all of the different national central banks’ funding activities in the market. For market participants, the credit line looks a lot like margin loans, however the ECMS credit line is automatic cash. With margin lending, banks know they have the credit line and ask for the cash but this process will be automatic under ECMS.

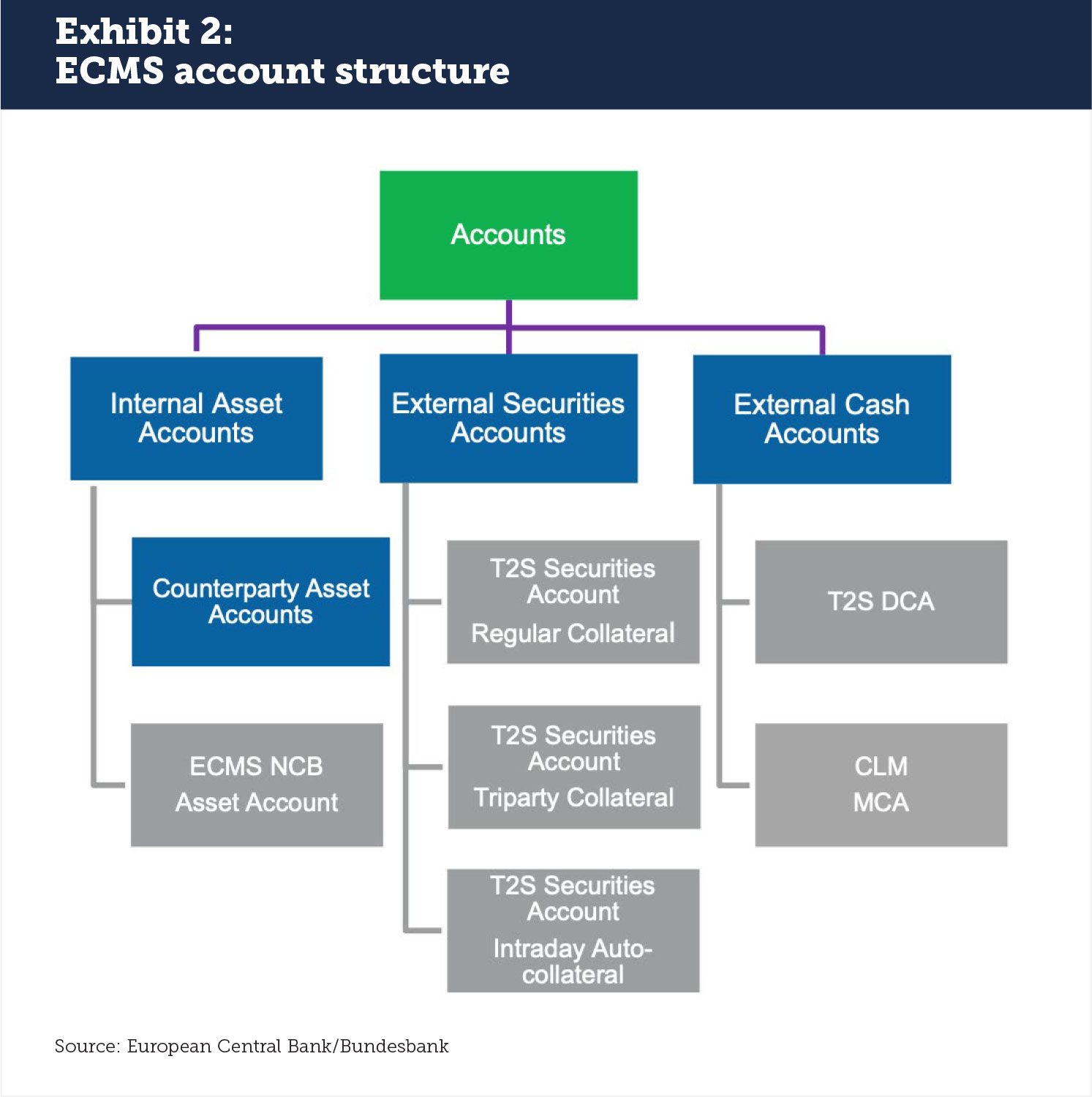

There are two places where the ECMS can access cash: as an internal counterparty asset and as an external account (see Exhibit 2). Internal assets are accounts opened in ECMS directly and used to track collateral positions in a Main Cash Account (MCA). External accounts are used by the ECMS to settle positions, provide intraday liquidity and send payment instructions, although ECMS does not track the cash balances of each participant. Cash collateral is mobilized at 17:00 when non-cash collateral is unavailable with a debit to the MCA, which is how monetary policy operations, cash collateral payments, and corporate action payments within the ECMS will get settled. The process is reversed the next business day (19:00-19:30) so long as other collateral is available.

For both securities and cash accounts, the fact that ECMS will have access means that funding and settlement managers must be aware of the assets in those accounts at all times. ECMS creates a hidden funding risk of being overdrawn or failing to deliver on time, which will result in fees from lines of credit and lost interest on cash. Both securities and cash accounts for ECMS use can no longer be tabulated by what is left at the end of the day; they must be actively utilized to ensure a positive result.

Margin loans are still recognized in ECMS although they are a separate account entry recognized as “marginal lending”. Marginal lending on request is conducted with immediate settlement while automatic marginal loans are processed at the end of the day in TARGET2. Institutions will need to be aware of what is in their cash account, which may look like a margin loan for operational processing, and what the ECMS calls marginal lending.

Executing on Cash Management Under ECMS

The use of technology that tracks, accounts for and supports the use of cash accounts will be the only way that banks can take advantage of the opportunities and protect themselves from the hidden risks of ECMS. Cash will be an asset class that must be supported in that technology system. Murex is prepared for this new development with its cross-product and cross-asset platform that can already represent the P&L of the cash pool; ECMS aligns to Murex’s existing MX.3 offering. As Murex’s Farhat pointed out, “Murex’s strength is that we are not only a lending solution, a Delta One nor a repo solution: we are all of those together. Likewise, fixed income and equity are joining forces under ECMS, which Murex already does. This gives our clients the alignment already that ECMS is going to deliver.”

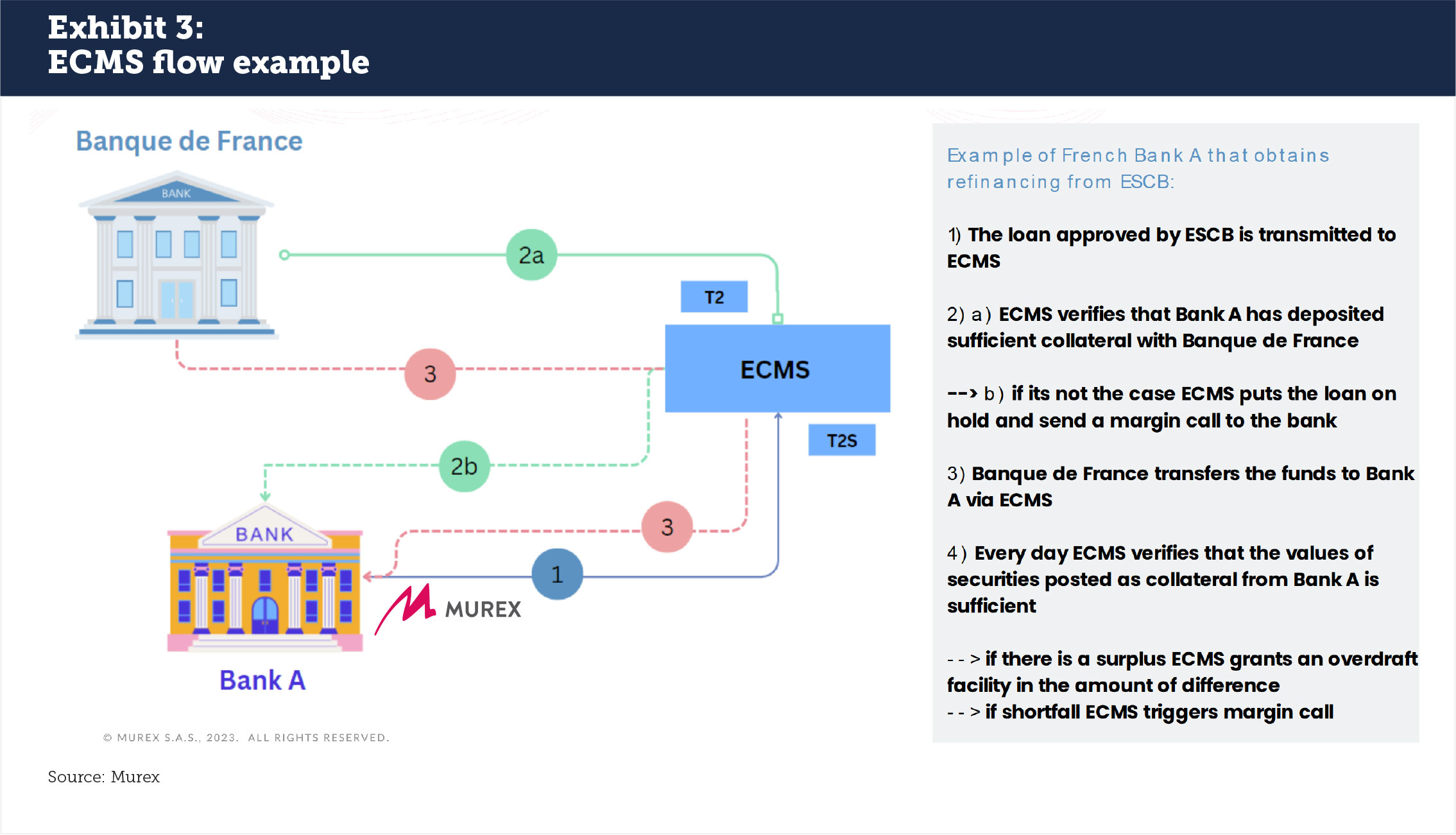

In an example of how ECMS will work, Bank A requests a loan from the European System of Central Banks (ESCB) using Murex technology that accounts for securities and cash, credit and debit accounts (see Exhibit 3). The approved loan is transferred to ECMS from its national central bank for the account of Bank A. ECMS verifies daily that Bank A is meeting its collateral obligations and sends margin calls as needed to the central liquidity management tool. These margin loans may need to be reported to trade repositories under the Securities Financing Transactions Regulation (SFTR), another area where technology is required and Murex is already enabled to deliver.

According to Farhat, “Murex’s catalog of all types of financing products can already be used to represent ECMS in the system. This includes management of triparty accounts, where national central banks can initiate transactions using existing counterparty transaction IDs.” This means that ECMS may use the collateral and avoid freezing or claiming cash in some circumstances, which would mean lost interest in a positive interest rate environment. Since ECMS will be able to communicate directly with triparty agents to access cash and collateral, individual banks must track and supervise that activity as well to avoid errors.

The introduction of ECMS represents a broad new stage of advancement for European capital markets and will ultimately be an important way for Europe to achieve Capital Markets Union. However, there are intermediate steps that may be uncertain for market participants as they adapt to the new technology and the new way of managing cash and securities as collateral. Farhat notes that “Starting with a robust technology platform that already sees collateral the way that ECMS does – cross-product, cross-silo and cross-asset class – is the best way to start out. Murex looks forward to working with its clients to support their transition to the ECMS environment.”

This article was commissioned by Murex.

About Murex

Murex provides enterprise-wide, cross-asset financial technology solutions to capital markets players. With more than 60,000 daily users in 65 countries, its cross-function platform, MX.3, supports trading, treasury, risk and post-trade operations—enabling clients to better meet regulatory requirements, manage enterprise-wide risk and control IT costs. Learn more at www.murex.com.