The December 2014 Senior Credit Officer Opinion Survey (SCOOS) on Dealer Financing Terms has been released. As is usually the case, the interesting parts are the special questions.

Before getting into the special questions, there was one issue that caught our eye.

From the questions on counterparty types:

“…Hedge Funds. About one-fifth of the respondents to the December survey indicated that the price terms (such as financing rates) offered to hedge funds for securities financing and OTC derivatives transactions tightened somewhat in the past three months. The most cited reason was the diminished availability of balance sheet or capital. (emphasis added) By contrast, dealers indicated that nonprice terms (including haircuts, maximum maturity, covenants, cure periods, cross-default provisions, or other documentation features) were basically unchanged over the past three months…”

The rationing of balance sheet and its impact on repo gets a fair amount of press, so it isn’t a big surprise to see it show up in the SCOOS. On the other hand, the “one-fifth of the respondents” represents 4 survey participants out of the 22 who answered the question (the other 18 all said “remained basically unchanged”). When the same question was asked to Mutual Funds, Exchange-Traded Funds, Pension Plans, and Endowments, all 22 respondents said, “Remained basically unchanged”. For Insurance Companies, 1 answered, “Tightened somewhat” and 21 said “Remained basically unchanged”. Are hedge funds the first to lose access to financing or just the clients who use it the most?

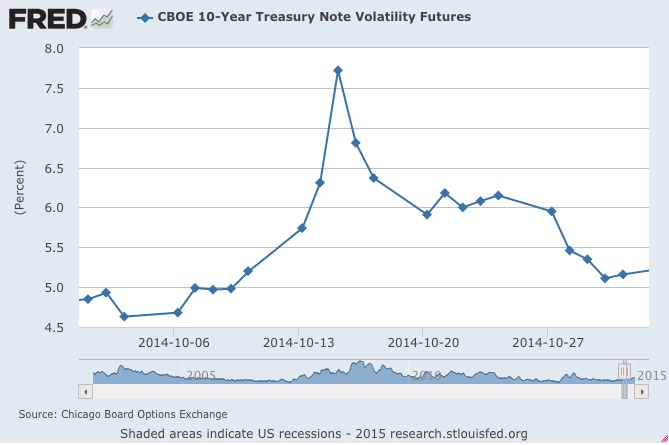

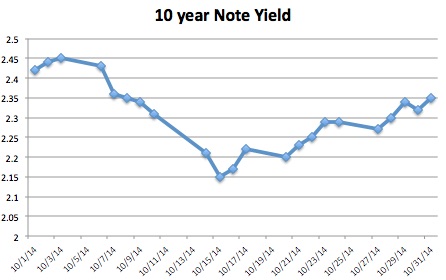

On the special questions: the focus was on October 2014, a period of high volatility. The Fed wanted to know how clients changed their portfolios and if margin requirements on derivatives went up during that period. As a reminder, this is what the market looked like then:

{kind=link}

{kind=link}

Source: US Treasury

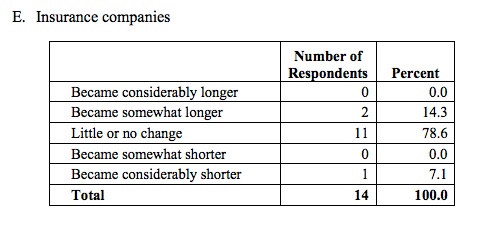

The survey asked if clients adjusted their portfolios during October, looking at the first half of October overall and then specifically on October 15th between 8:30am and 10:00am. Examining the narrow time frame, it turns insurance companies stayed pretty stable.

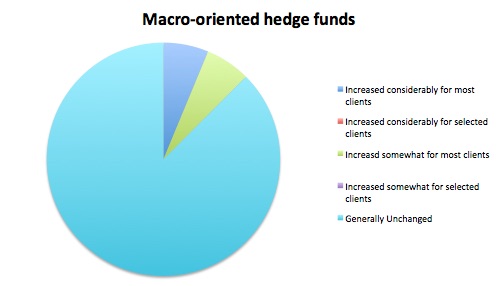

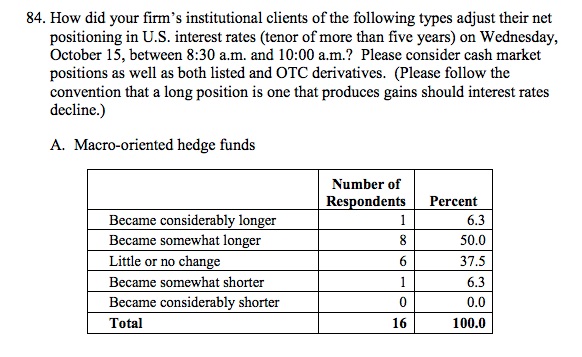

But hedge funds moved their portfolios around a fair amount.

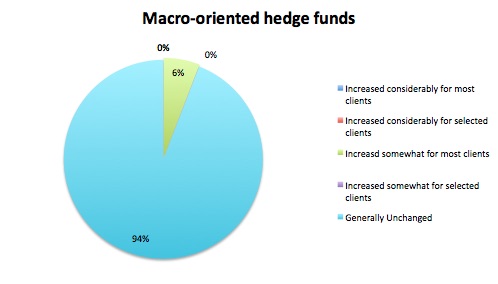

The second special question was about margin on derivatives trades. Considering the spike in volatility, were margins increased? The answer was largely “no”. This was true for both listed derivatives and OTC. For example, when asked about Macro Hedge Funds: “Did your firm adjust margin requirements applicable to OTC derivatives contracts referencing short- and medium-term U.S. interest rates on October 15 or in the days following?”

Source: http://www.federalreserve.gov/econresdata/files/SCOOS_201412.pdf

It is interesting that the Fed is asking the question in the first place. Did they expect banks to respond to the increase in volatility so quickly? Was it their way to express disappointment that banks didn’t have a quicker trigger finger (although that would be pro-cyclical behavior)? What would have happened if the volatility was sustained for a longer period or rates rose instead of fell? Lots of questions…