Simon Potter spoke at the SIFMA Conference on Securities Financing Transactions yesterday in New York. Potter is the Fed’s man in charge of open market operations and he explained how the Fed would accomplish normalization (a/k/a raise rates) when the time comes. His speech was entitled “Interest Rate Control during Normalization”.

Potter said that by raising rates paid on excess reserve (IOER), Fed Funds will go up.

“…when economic conditions and the economic outlook warrant a less accommodative stance of monetary policy, the Committee will raise its target range for the fed funds rate. During normalization, the Committee intends to move the fed funds rate into the target range primarily by adjusting the rate of interest on excess reserve balances (IOER) that it pays. We expect changes in the IOER rate to have a significant influence on the fed funds rate and other short-term interest rates. However, to help control the fed funds rate, the Committee also intends to use an ON RRP facility and other supplementary tools, as needed. The Committee will use an ON RRP facility only to the extent necessary, and will phase it out when it is no longer needed to help control the funds rate…”

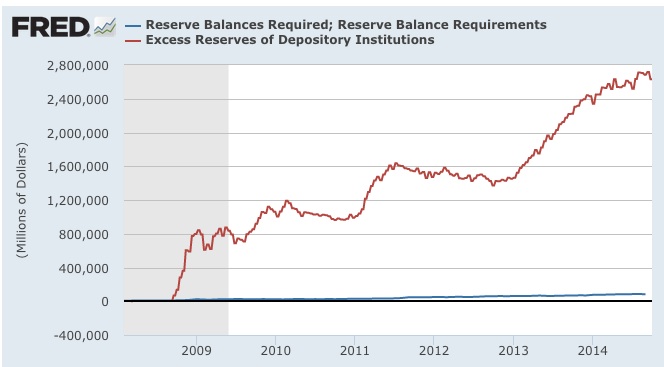

If the Fed’s objective is to raise the Fed Funds rate (when the time comes…), we wonder if the linkage between IOER and Fed Funds is strong enough. Fed Funds are the trading of required reserves. With QE, the system has been flooded with cash, creating an enormous excess reserve position. There just isn’t a lot of demand for required reserves. Potter said that Fed Funds trades about $60 bio a day – but that is paltry compared to excess reserve positions. It seems like the theory is: as the Fed’s QE assets fall, excess reserves will shrink and eventually demand for required reserves will come back, restoring the traditional relationship to Fed Funds. But the ratio of excess to required reserves is more than 30:1 and it will take a long time to unwind enough QE assets to make a difference.

Source: Federal Reserve Bank of. St. Louis, FRED

“… the FOMC has judged it appropriate to operate with a framework for interest rate control that is based primarily on administered rates rather than reserve draining tools…”

“…While the Committee has targeted the fed funds rate for many decades, activity in the fed funds market has changed considerably in recent years. Prior to the crisis, many banks typically borrowed fed funds in order to satisfy reserve requirements or obtain short-term financing. In recent years, however, the Fed’s LSAPs have led to very high levels of reserve balances, and thus reduced the need for banks to borrow fed funds to meet reserve requirements and clear payments. As a result, trading activity in the fed funds market today is smaller and the nature of that activity is different than it was prior to the crisis…”

“…During normalization, the Fed intends to move the fed funds rate into the target range established by the FOMC primarily by adjusting the IOER rate…”

IOER and RRP are administered rates, Fed Funds and GC rates are market driven. It seems like the Fed is relying on pushing up IOER to the point that banks will borrow in the Fed Funds market, driving the rate up, and deposit cash at the Fed at an even higher rate. Potter contended that IOER will act as a “magnet”, pulling short rates along with it. Frictional costs like FDIC insurance tend to dissuade domestic banks from doing the trade, but we suppose that if the IOER/Fed Funds spread got high enough, it could overcome the costs. However, while riskless, it still attracts balance sheet and capital. It may be hard to argue the return is worth the trouble. We think a more effective method will be to increase the RRP rates, which in turn will push dealers to increase GC levels. That will ripple through to all short rates on UST, GSE and corporate curves. It is more immediate and less dependent on the dysfunctional Fed Funds market and the “magnet” effect.

As an aside, we wonder if normalization will have the added benefit of eventually shrinking bank balance sheets (as excess reserves fall) and perhaps toning down some of the TBTF rhetoric….but at the risk of others sounding the alarm bell over the Fed subsidizing the Banks with this nice arb. You can’t win.