The Financial Stability Board (FSB) released its global monitoring report on non-bank financial intermediation (NBFI) for 2022. The NBFI sector exhibited strong growth in 2021, in large part because of higher valuations and inflows into investment funds, which benefited from the economic recovery.

The report covers 29 jurisdictions that account for around 80% of global GDP. The report mainly covers developments in 2021, during which most economies experienced a better-than-expected recovery from the COVID-19 shock, in many ways because of the extraordinary steps taken by official sector authorities to support key financial markets and the real economy.

Total assets

Driven mainly by the NBFI sector’s expansion, total global financial assets continued to exhibit strong growth in 2021, increasing by 7.7% to $486.6 trillion. The NBFI sector grew by 8.9% in 2021, higher than its five-year average growth of 6.6%, reaching $239.3 trillion.

The strong growth in central bank, bank, and public financial institution assets exhibited in 2020, in response to the outbreak of the COVID-19 pandemic, slowed down in 2021 in most jurisdictions. Accordingly, the total NBFI sector increased its relative share of total global financial assets from 48.6% to 49.2% in 2021.

NBFI sector growth in 2021 was, once again, mainly driven by investment funds, particularly equity funds. The growth in investment fund assets was supported by a combination of flows and valuation effects, with equity funds’ growth driven mostly by increases in valuations during 2021.

Growth in other investment fund assets, i.e. excluding hedge funds, real estate investment trusts and real estate funds (REITs), and money market funds (MMFs), accounted for just over a half of the overall change in NBFI sector assets, while insurance companies and pension funds were collectively responsible for a quarter of NBFI sector asset growth.

While large data gaps remain, OFIs continued to have the largest cross-border linkages across sectors. In 2021, NBFI entities’ interconnectedness with the banking sector continued to decrease. This trend has been observed since 2013 both in terms of funding and exposures.

The narrow measure of the NBFI sector grew by 9.9% to $67.8 trillion, representing 28.3% of total NBFI assets and 14.1% of total global financial assets. The narrow measure, which reflects an activity-based “economic function” (EF) assessment of risks, includes the following elements:

- Collective investment vehicles with features that make them susceptible to runs (EF1) grew by 10.6% in 2021, representing 76.2% of the narrow measure. Measures of credit intermediation and liquidity transformation for non-government MMFs and fixed income funds remained at elevated levels. Measures of maturity transformation for fixed income funds also remained at elevated levels.

- Loan provision that is typically dependent on short-term funding (EF2) grew by 7.7% in 2021, representing 6.8% of the narrow measure. Measures of maturity transformation, leverage and liquidity transformation largely resembled those in 2020, albeit with notable declines in the maximum values of these distributions.

- Intermediation of market activities dependent on short-term funding (EF3) grew by 5.6% in 2021, representing 6.8% of the narrow measure. Risk metrics all decreased in 2021.

- Insurance or guarantees of financial products (EF4) grew by 4.0% in 2021, representing 0.2% of the narrow measure.

- Securitisation-based credit intermediation (EF5) grew by 9.0% in 2021, representing 7.5% of the narrow measure.

- Assets that are unallocated between the five EFs represent 2.4% of the narrow measure.

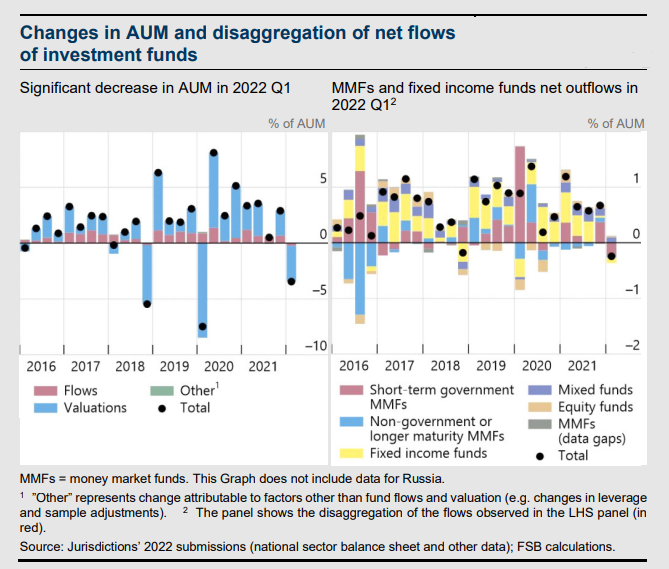

In early 2022, macro-financial conditions changed dramatically with the war in Ukraine, market volatility and commodities’ price pressure. In addition, continued supply-chain difficulties contributed to concerns that inflation could become more persistent than expected. The report also takes stock of the situation in which the NBFI sector entered the year 2022 and provides insights on how vulnerabilities could develop given the changing macro-financial conditions. For example, investment funds suffered a significant decrease in the value of their assets under management (AUM) in the first quarter of 2022 primarily because of valuation effects, although net outflows were also historically high.