ICMA today released two documents on the repo market. The first was an analysis of proposed CSDR mandatory buy-in rules. This is a highly contentious issue and the ICMA is justifiably concerned about the impact on bond and repo liquidity, costs and the potential to reshape the repo market. The second was the biannual European repo survey, which showed the beginnings of the Leverage Ratio’s impact on repo volumes.

ICMA Impact Study for CSDR Mandatory Buy-ins

Why get concerned about mandatory buy-ins? According to ICMA:

The provision for mandatory buy-ins will supersede the current rights of a counterparty to a non-cleared financial transaction who, at their discretion, can force delivery of securities (or cash) in the event of a settlements fail. Rather than buy-ins being a contractual remedy available to a failed-to counterparty, under CSDR it will become a mandated obligation of the failed-to counterparty, the chosen place of settlement (the CSD), or even the trading venue on which the transaction was executed.

Speaking at the ICMA’s press conference yesterday in London, Andy Hill, director, market practice and regulatory policy, said that the mandatory buy-in provision of the Central Securities Depository Regulation (CSDR) could cost bond markets over €30 billion and repo markets over €2 billion if implemented. “This could kill the term repo market,” he said.

The expectation is that not only will direct costs increase but that unknown costs and risk will increase as well. According to the European Central Securities Depositories Association (ECSDA), mandatory buy-ins ” would result in over 1.8 million buy-ins being executed per annum, representing a total transaction value of €2.5 trillion. To adjust for this additional risk and potential cost to their service, market-makers will be forced to add a premium to their market offers, or may simply choose not to show offers in certain securities.” The expectation is that liquidity will significantly decrease as market-makers avoid the uncertainty risk that mandatory buy-ins would bring.

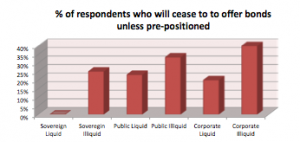

The ICMA study took this argument a step further by surveyed market makers on the impact of mandatory buy-ins on bond market bid-offer spreads and how many market-makers would leave the market altogether unless pre-positioned (see graphic). A partial summary of their findings by product type is:

Bonds % spread increase % ceasing to offer

Sovereign Liquid 116% 0%

Sovereign Illiquid 120.7% 25%

Public Liquid 120.3% 23%

Public Illiquid 74.4% 33%

Corporate Liquid 155.2% 20%

Corporate Illiquid 99.3% 40%

Repo % spread increase % ceasing to offer

Sovereign Liquid 183.6% 0%

Sovereign Illiquid 149.3% 33%

Public Liquid 166.6% 6%

Public Illiquid 90.9% 40%

Corporate Liquid 153.9% 12%

Corporate Illiquid 133.8% 60%

Other comments from the press conference:

Andy Hill labelled the legislation unimplementable and unmanageable. The CSDR was passed into law in the second half of 2014, and the mandatory buy-in regulation is scheduled to come into force in early 2016.

Godfried de Vidts, chairman of ICMA’s European Repo Council, said that drawing in CSDs, and ATSs into the buy-in was “against the MiFID spirit of competition between ATSs and CSDs”. He called for a mechanism like the no-action relief in Dodd-Frank to be implemented in Europe to allow parties to reach a technical solution.

“If this (mandated buy-in) is implemented by June 1 2016 it is creating unsafe markets instead of making them safe,” said de Vidts.

Key findings from the European repo survey

This survey of the amount of repo business outstanding on 10 December 2014 sets the baseline figure for market size at €5,500 billion, (€5.5 trillion) representing a decline from the figure of €5,782 billion recorded in the last survey in June 2014. Using a constant sample of banks who have participated in the survey over the long term, it is estimated that that the market has shrunk by at least 4.8% since June and by 2.8% since December 2013.

Other highlights:

- The Leverage Ratio has begun to be a major constraint on balance sheets and addition to the cost of business.

- The impact of regulation appears to be greatest on commoditized, short-term, interdealer repos of government bonds.

- Central clearing has been a top priority for major banks.

- The average maturity of business lengthened, reflecting in part seasonal longer-term financing to bridge the end of the year but possibly regulatory pressure to seek more stable (ie longer term) liabilities.

- There are various indications of increasing collateral transformation as banks swap collateral to acquire the high-quality liquid assets (HQLA) required by new regulations.