How Can Participants Benefit?

Over the past decade, the clearing landscape has been transformed. Central counterparty (CCP) innovation, driven in part by regulatory change, has led to efficiencies from clearing (as the corresponding costs of bilateral activity have increased), better customer protection and integrated workflows that enable efficient risk management.

Extending Access

More recently in Europe and the UK, Sponsored Clearing has opened the door to the buy-side, providing an additional route to repo liquidity. This enables buy-side firms to have direct relationships with CCPs via agent member banks.

Sponsored Clearing is becoming an important consideration within the range of tools available to buy-side repo market participants and is a key driver for the expansion of the repo market ecosystem — creating a ‘virtuous circle’ effect by attracting an increasing range of eligible participants to the CCP. Crucially, it further deepens the liquidity pool, which provides the potential for better pricing from dealers, offers more opportunities for margin and balance sheet availability, and ensures access and diversity for liquidity managers at buy-side firms.

Awareness of the benefits of clearing, particularly for market participants that have not been engaged in clearing, are now rippling across the industry.

Industry developments

The US market was the first to adopt sponsored repo clearing at FICC (a DTCC company), which supported the regulatory objectives of increasing access to and adoption of clearing, and of gaining a centralised view of the risk carried by the market.

However, following COVID-19-driven turbulence in the US Treasury market in March 2020, regulators and industry bodies are turning their attention to additional instruments that should be considered for clearing.

Among these is the Group of Thirty Working Group on Treasury Market Liquidity (G30), an influential think tank of policymakers and market practitioners, which in 2021 published recommendations in its US Treasury Markets report for improving the resilience of this market at a time of increasing government bond issuance.

The report urges US regulators to make it easier for principal trading firms (PTFs) to clear US Treasuries at FICC, which was established after the failure of several Treasuries dealers in the 1980s. This could lead to both cash bonds and an increasing proportion of repo trades clearing.

The G30’s position is supported by DTCC, which references the report and highlights the benefits of more securities being cleared through CCPs in a recent industry white paper. The paper, which considers the benefits of clearing in the US Treasury market and FICC’s approach to it, signals that the direction for global repo (and outright) markets is towards clearing, with a much wider participant base.

In light of the broad consensus on the benefits of increased central clearing of US Treasury transactions, the focus should now turn from whether to adopt a clearing mandate to how to implement such a mandate, including, among other questions, whether the cleared U.S. Treasury market ought to more closely resemble the cleared swaps market before a U.S. Treasury clearing mandate is implemented.

Making the U.S. Treasury Market Safer for All Participants: How FICC’s Open Access Model Promotes Central Clearing (DTCC, October 2021)

Equally, a recent SIFMA paper re-quoted Stanford University economist Darrell Duffie on the topic of central clearing in the US Treasury market:

Darrel Duffie has argued…that a broad central clearing mandate ought to be considered because ‘the size of the Treasury markets will outstrip the capacity of dealers to intermediate the market’. In his view, greater central clearing could free up ‘the amount of dealer-balance sheet space necessary to maintain liquid markets’.

Evaluating the Benefits and Costs of Central Clearing in the Treasury Markets

(SIFMA, November 2021)

These discussions and papers lead to the obvious question of how the UK and Euro markets should prepare for these increasingly strong arguments towards buy-side repo clearing.

Prepare by building access

The G30 report, while focused on the US market, notes that the principles discussed for clearing US Treasuries are applicable to other world bond markets. While these principles may take time to spread globally, there is no doubt that clearing delivers fundamental economic and systemic risk benefits.

Banks are increasingly looking to become more efficient and optimise their balance sheet and collateral management, whilst the buy-side wants to reduce repo financing costs and secure access to reliable repo capacity/liquidity pools. These factors therefore encourage repo market participants in the UK and Europe to further build access to cleared repo by connecting to services such as LCH RepoClear’s Sponsored Clearing (available in both Euro and Sterling debt).

The buy-side benefits of repo clearing

Repo clearing benefits the entire repo market by providing access to deep liquidity, settlement efficiencies and enhanced risk management — and a larger ecosystem means greater benefits for all participants, including the buy-side.

The cleared environment is seeing increased volumes — a trend that authoritative industry voices believe will continue. Buyside benefits include:

- Best Execution: Buy-side firms are increasingly looking to embed access to clearing1 as soon as possible to enable a plethora of benefits, such as the ability to assess whether the best execution price (net of the full cost of clearing) is within the cleared environment.

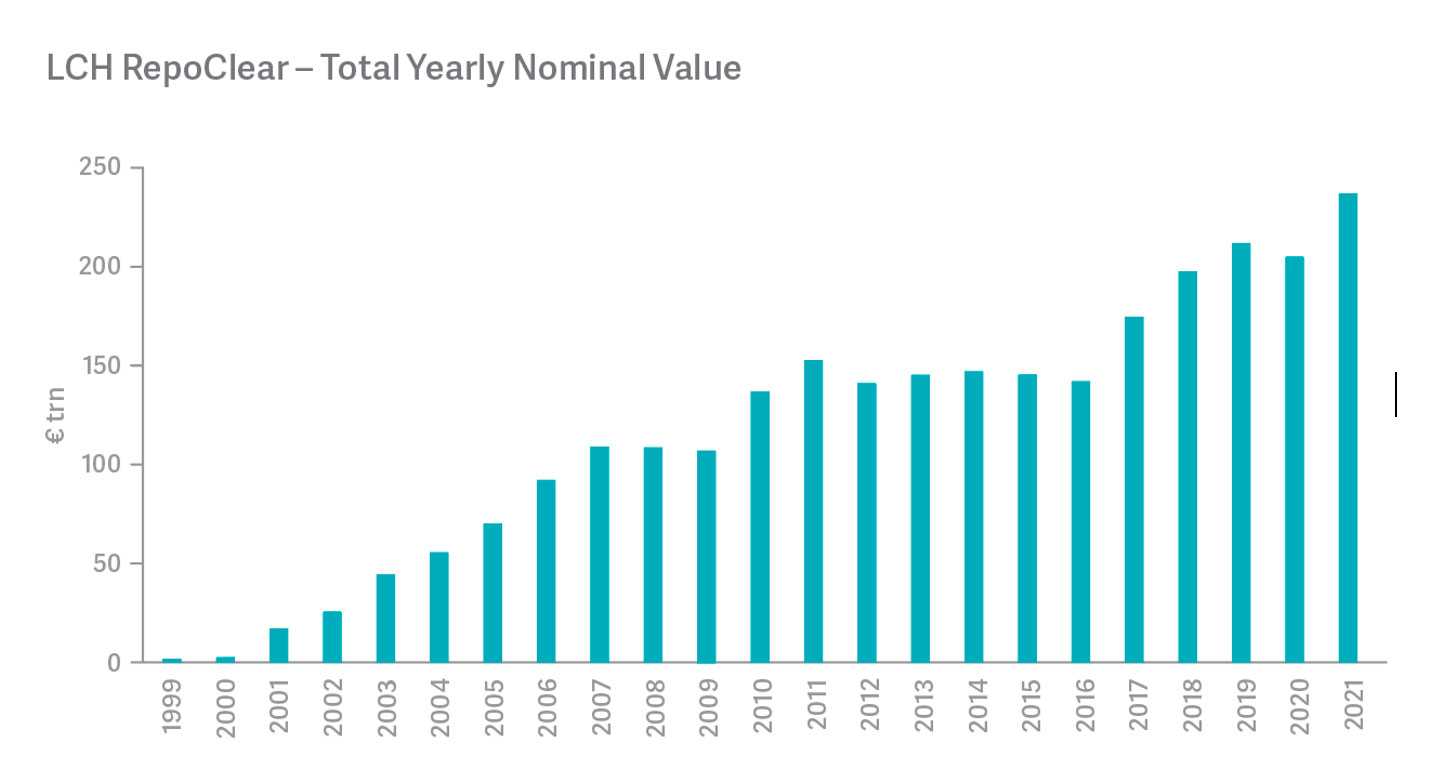

- Liquidity: Buy-side firms can take advantage of liquidity that is available now through clearing, and ensure access for future needs — such as the liquidity requirements that could arise from pension schemes being required to clear OTC derivatives from June 2023 — by establishing multiple, open access points to liquidity pools. RepoClear is connected to a broad range of trading venues and settlement locations, providing extensive choice, and builds connections where users need them. Offering deep liquidity and multiple connectivity choices simultaneously is the core strength of the RepoClear service. In fact, the service is already trusted by over a hundred members, which cleared over €237 trillion of nominal in 2021 across Euro debt and UK Gilts.

- Settlement Efficiencies: CCP settlement netting decreases settlement and liquidity risk by reducing the physical movement of securities and cash by over 70% compared to the uncleared market. This translates into material operational and cost efficiencies.

The buy-side’s next step?

In Europe, just over 50% of the government bond repo market is cleared, the majority of which is dealer-to-dealer, with a small but growing amount of dealer-to-client business. Twenty-seven buy-side funds now are live and able to clear Gilts at RepoClear. The above points to more market participants (including buy-side firms) choosing to adopt clearing for an ever-greater proportion of their repo clearing. This includes dealer members in the Americas and APAC, who are contributing to record volumes and the global expansion of the service.

Looking to the future

RepoClear’s long-standing, collaborative partnership with both members and regulators allows us to continually develop efficient and innovative solutions that also reduce systemic risk.

- Innovation: Working in close partnership with the market, LCH continues to innovate to enable a broader range of buy-side firms to access cleared repo, alongside the existing PSAs, LDIs, MMFs and regulated funds that are already clearing. This includes collaboration to develop a workable guaranteed Sponsored Clearing model, which, subject to internal governance and regulatory approval, will extend access to certain categories of alternative investment funds, allowing them to benefit from clearing liquidity pools that reduce risk and increase efficiency as a result of their size.

- Optimisation: At RepoClear, we know that optimisation is more critical than ever, which is why we are continuously improving our margin model (VaR-based)2. These initiatives serve to further increase margin efficiency, enabling users to minimise costs and free up resources to adapt to the new market dynamics, in partnership with their CCP.

- Wide Range of Acceptable Collateral: Continuing the theme of optimisation, LCH has worked to extend the eligible securities collateral that are accepted, with members now able to pledge a wider range of securities against their LCH margin requirements, with recent examples being Singaporean and Norwegian government bonds.

- Constant Improvement: Regulatory developments, unpredictable market conditions and the ever-shifting macroeconomic environment continue to create new challenges for repo market participants. CCP participants’ evolving needs are a key driver of product innovation at RepoClear. With this in mind, LCH plans to merge2 €GCPlus, a general collateral (GC) product, with RepoClear’s Euro government bond clearing service to deliver greater efficiencies and a nettable set of options for the user — all in one place.

- Listening and Acting: Our members and their clients have told us that efficient resource management and optimisation are growing priorities. To address this, LCH has developed a suite of data, analytics and optimisation services that increase efficiency and reduce costs across the trade life cycle. This includes tools that improve settlement performance using trusted data and analytics. As the markets’ partner, we stand ready to co-pilot the use of our services with our members and clients.

‘We are pleased to be the first Sponsored Member to clear

a euro repo trade at RepoClear SA. This initiative by LCH is important for the market, as it provides buy-side members

access to LCH RepoClear’s liquidity pool, enabling better risk management, stability and operational efficiencies’.

– PGGM

Delivering value to the market

RepoClear has an unwavering focus on delivering value to members and clients, whose needs are constantly evolving as market dynamics shift.

Access to the large and stable netting pool that clearing provides is a key advantage for banks. RepoClear enables netting across 14 cleared markets in Europe (plus the UK), in addition to two GC pools, Term £GC and €GCPlus, the latter of which will, in 2022, be merged2 with the RepoClear service to deliver even more balance sheet and margin efficiency gains.

For both the sell-side and the buy-side, RepoClear offers significant choice and benefit, which is why building access to the service is, increasingly, a priority. Buy-side Sponsored Members gain access to a huge number of execution counterparties with a single membership of the CCP, and buy-side eligibility continues to expand. The more buy-side clients adopt Sponsored Clearing, the better the balance sheet netting opportunity for dealers and the potential for greater balance sheet capacity for the buy-side — a ‘win-win’ for the entire repo market ecosystem.

1‘Cleared Repo is helping control costs for pension funds’. Insight Investment, December 2021 2Subject to final regulatory approval