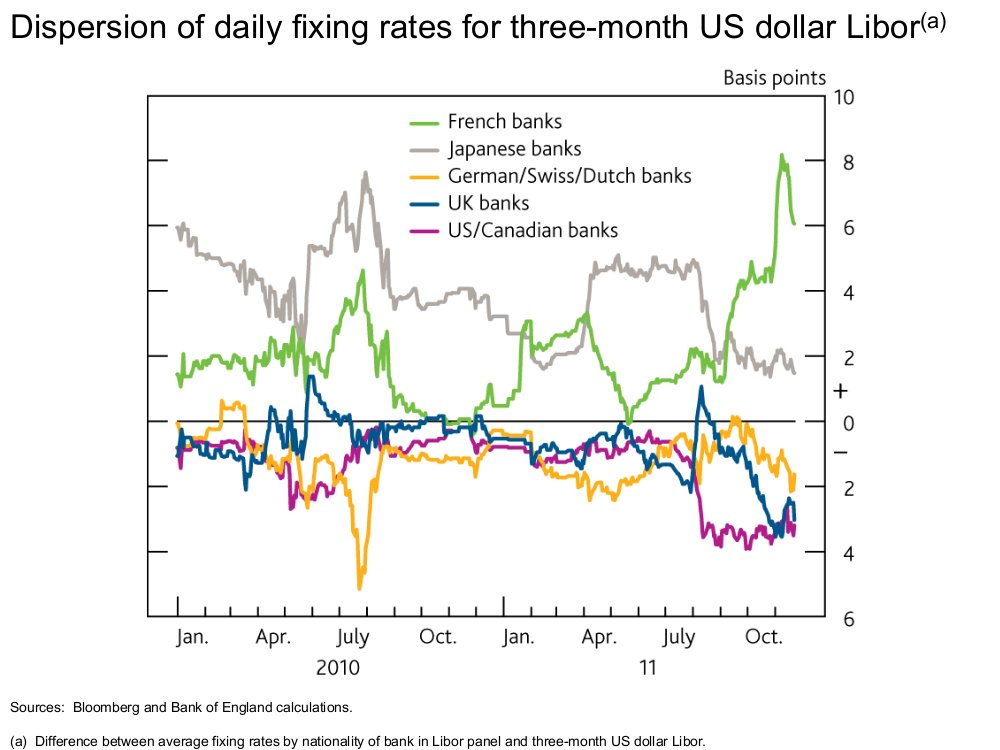

For fans of the data that underly widely quoted statistics and assumptions, the new Bank of England Financial Stability Report provides a trove of worthwhile information. One of the more interesting parts of the report is data on what bank rates have been driving LIBOR. As it turns out, there has been above-average risk in French banks relative to LIBOR, the US, Canada, Germany and Japan. And here the French government is angry at the ratings agencies…

The graph below shows the average distance from 3 month LIBOR for each group of national banking institutions. In Q4 2011 French banks were requiring 4 to 8 basis points over 3 month LIBOR to fund their activities. While this may not seem like a lot, at the end of October 2011 3 month LIBOR was 42.9 bps and French banks were 8 bps over that figure. This is an 18.6% premium over the average. The overage declines to 6 bps in November 2011 and even though 3 month LIBOR is up over this month, French banks still require more than a 10% premium.

The risk perceived in funding French banks can also be linked to conversations that the French government has had with S&P and Moody’s. Following a leak to clients in early November, this week S&P is rumored again to plan a downgrade in French debt. Moody’s is also concerned.

Looking at the LIBOR detail, both the French government and French banks have a problem in how their risk is perceived. The French government can rail against the ratings agencies (and has) but market perceptions of risk are harder to quell.