Cash investors know that peer to peer (P2P) trading in repo can result in price improvement. This analysis quantifies the performance change for three popular US money market funds if they were to move their bilateral, Sponsored Repo and Reverse Repo Facility repo transactions onto the Venturi platform, and measures that change against peer rankings. The results show that P2P transactions on Venturi can support funds in beating industry benchmarks.

Venturi is a new P2P solution from State Street. Launched in November 2022, the platform offers buy-side firms access to other buy-side sources of liquidity via repos and reverse repos. As part of its P2P program, State Street guarantees the payment of the Repurchase Price to the cash lender to mitigate losses from a cash borrower’s default. State Street notes that S&P has reviewed the terms of the guarantee and affirmed that it meets S&P’s principles for credit substitution of an unrated counterparty.

Gino Timperio, global head of Financing Solutions at State Street, said that “As a result of elevated market volatility and the changing liquidity and rate environment, buy-side firms are increasingly seeking new and diversified sources of financing…. Venturi will empower our clients to discover new liquidity pools and make better, data-driven investment decisions.”

In Q2 2023, the platform is seeing increased traction among a variety of types of cash and collateral investors including money funds, pensions and hedge funds. State Street designed Venturi to streamline both trade negotiation and operational workflows associated with P2P transactions, accommodating a broad range of firms in the offering. While any cash or collateral investor could theoretically use the platform, in practice the funds with the greatest volumes or that require the most diversity in their funding sources are first movers.

Initial indicators are that when buyside firms interact directly backed by State Street’s credit guarantee, Venturi P2P transactions are providing price improvement for both cash and collateral providers. State Street reports that clients are seeing four bps improvement on US Treasury (UST) repo trades over bilateral and a bit less on Sponsored Repo UST bilateral. The improvement for agency repo can be larger, at six basis points. Given these figures, if an entire money fund portfolio moved to Venturi, how would that impact the fund’s performance vs. its peers?

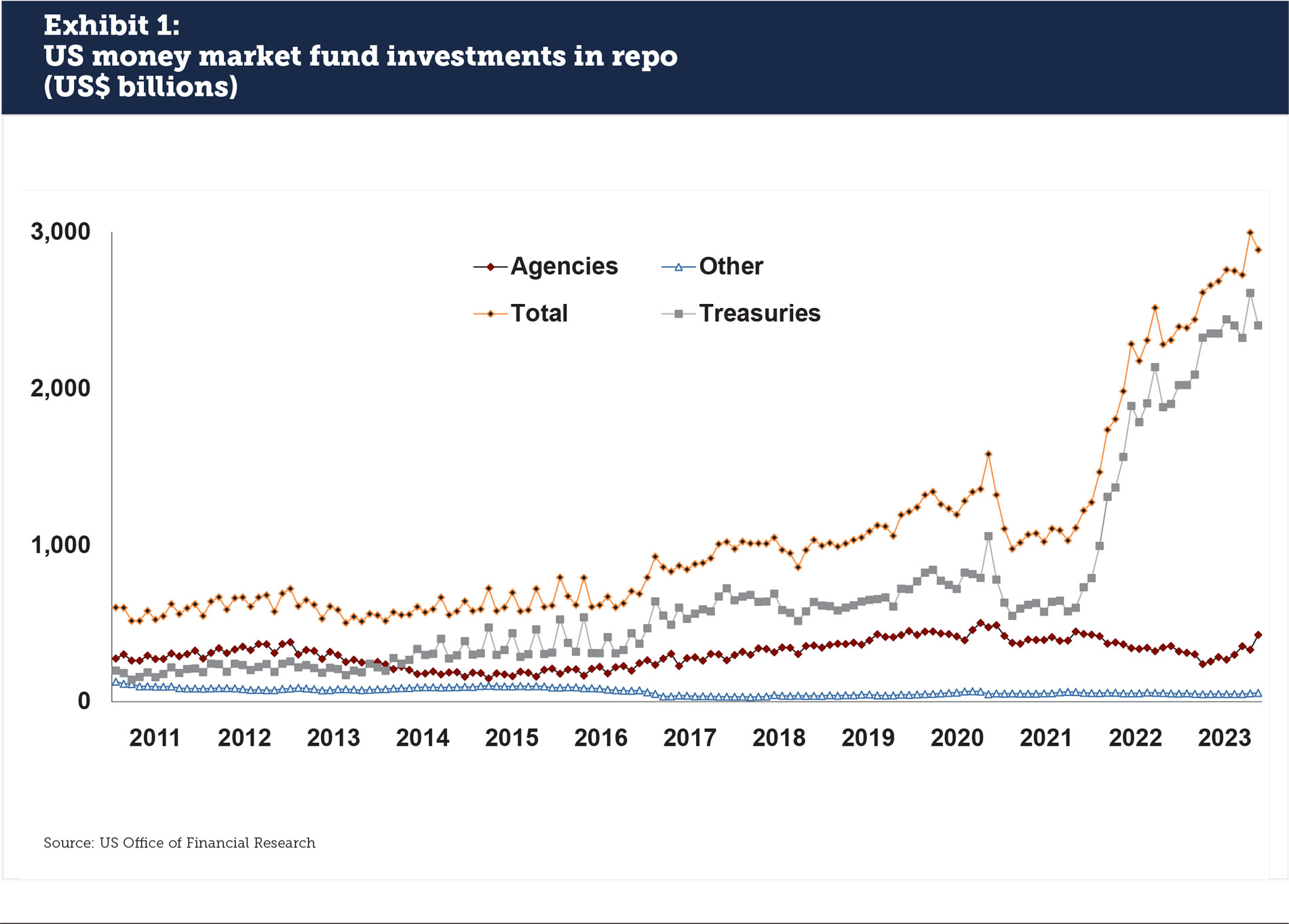

Money funds in the repo market

US money market funds are leading investors in the repo markets but this was not always the case. Fund investments doubled in repo from 2011 to 2019 as quantitative easing put more cash into the financial system, then tripled between 2021 and 2023, according to data from the US Office of Financial Research (OFR) (see Exhibit 1).

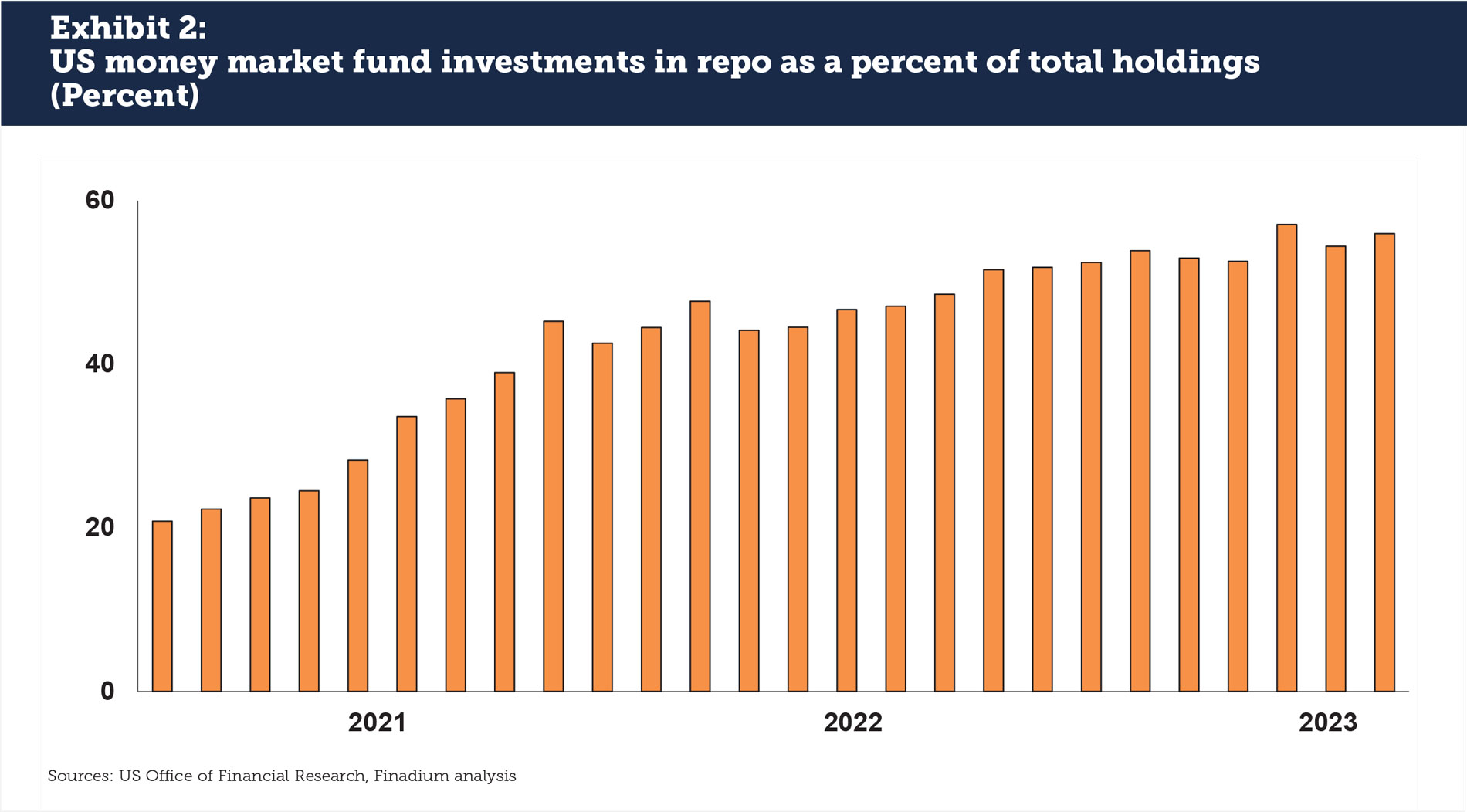

Repo has become a popular investment instrument with the availability of the Federal Reserve’s Reverse Repo Facility (RRP) and bank balance sheet dynamics that primarily have kept other money market instrument rates below the Fed’s benchmark level. OFR data show that repo comprised 56% of all US money market fund investments in February 2023, up from 20% in January 2021 (see Exhibit 2). The RRP was the counterparty to 83% of US Treasury, bilateral bank exposure was 11%, and bank exposure novated on the Fixed Income Clearing Corporation’s Sponsored Repo program was 6%. Transactions with non-bank peer counterparties was 0.4%.

Price improvement considering the State Street guarantee

In our conversations with large US money fund managers, we found interest in the Venturi P2P proposal and awareness that the State Street guarantee brings with it different dynamics than current bilateral or triparty repo procedures. The main concern is about counterparty credit risk and what happens in the event of a default in the guarantee process. State Street notes that it has engaged closely with cash investors, including large US money fund managers, regarding the program guarantee and would perform to the cash investor, taking on counterparty credit risk to the cash borrower. As a custodian with a market leading securities lending business under the same leadership, State Street is experienced in playing the role of liquidation agent and administering on guarantees or indemnities.

Some fund managers have determined that while they are attentive to the operations, there are no real obstacles to going live. Others will need greater assurances or to watch a default process play out first.

The impact of spread improvement on Venturi

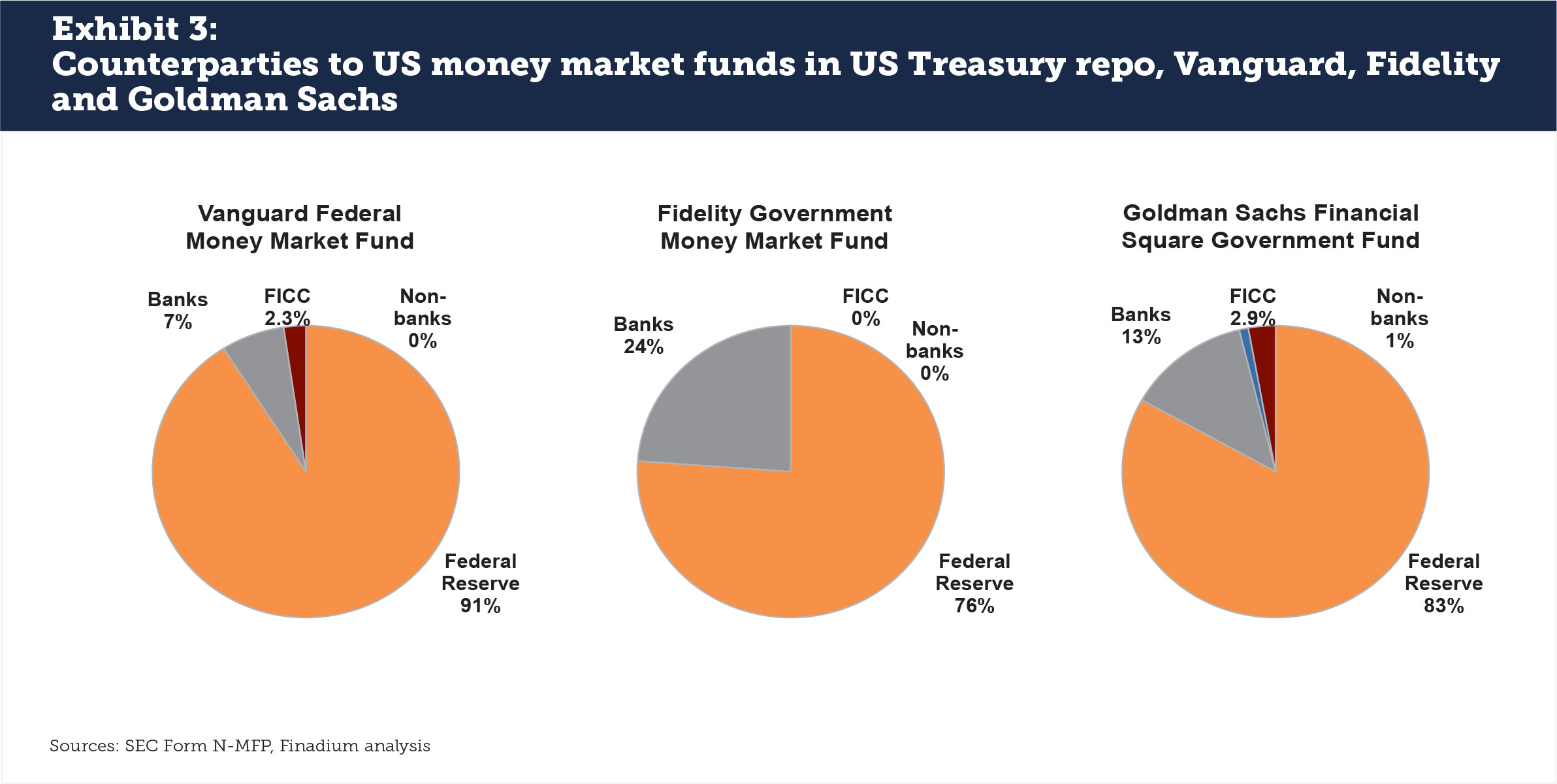

To test the utility of the Venturi P2P platform and how much impact it could have for US money market funds, we assessed the returns and repo exposure of three leading individual funds. The Vanguard Federal Money Market Fund, the Fidelity Government Money Market Fund and the Goldman Sachs Financial Square Government Fund are among the largest investors US Treasury and US Agency Repo assets in the money fund space; together, they hold over $750 billion in assets. Their individual exposures are predominantly at the Federal Reserve’s Reverse Repo Facility: Vanguard had 91% exposure, Fidelity 76% and Goldman Sachs 83% (see Exhibit 3).

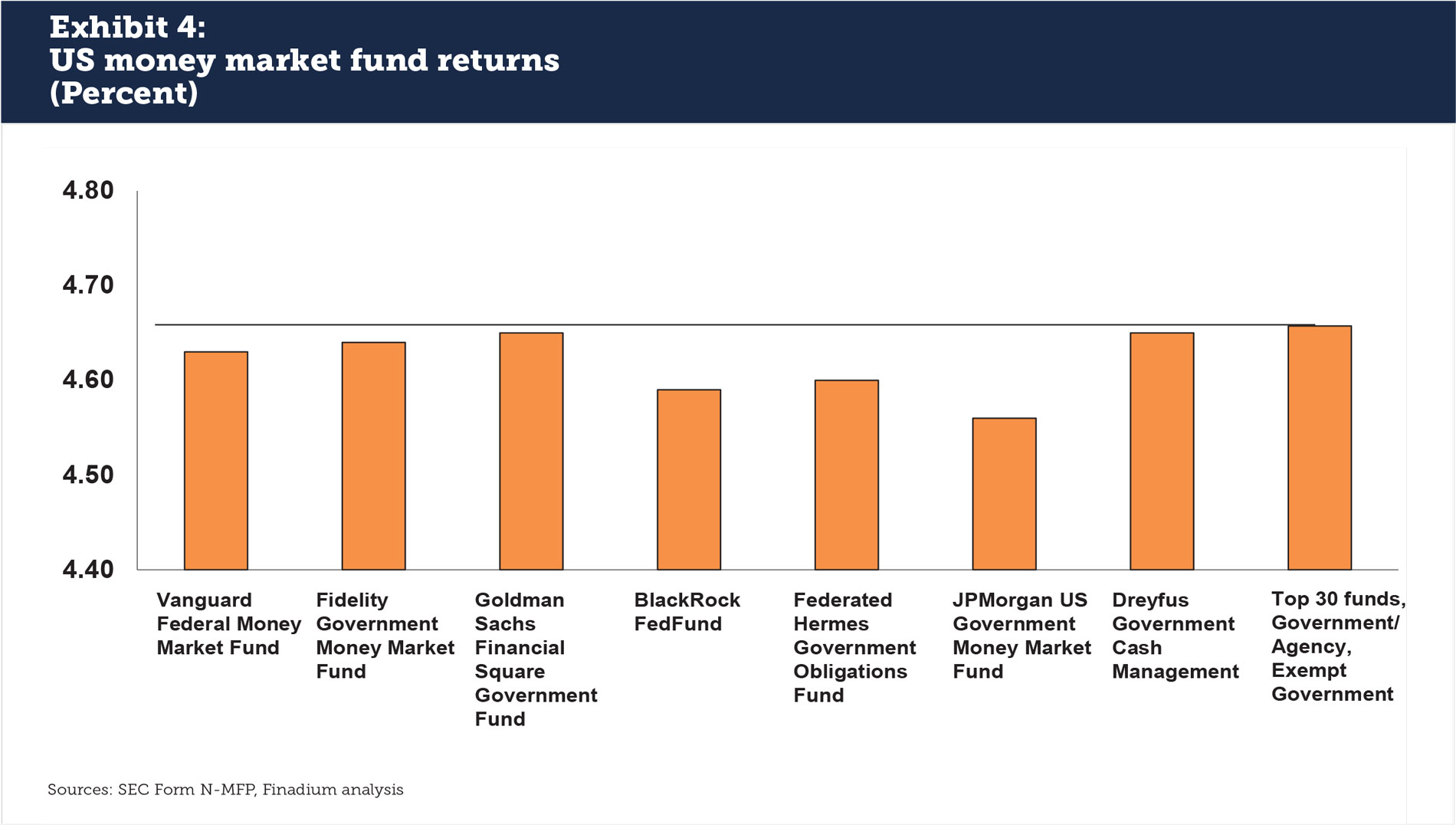

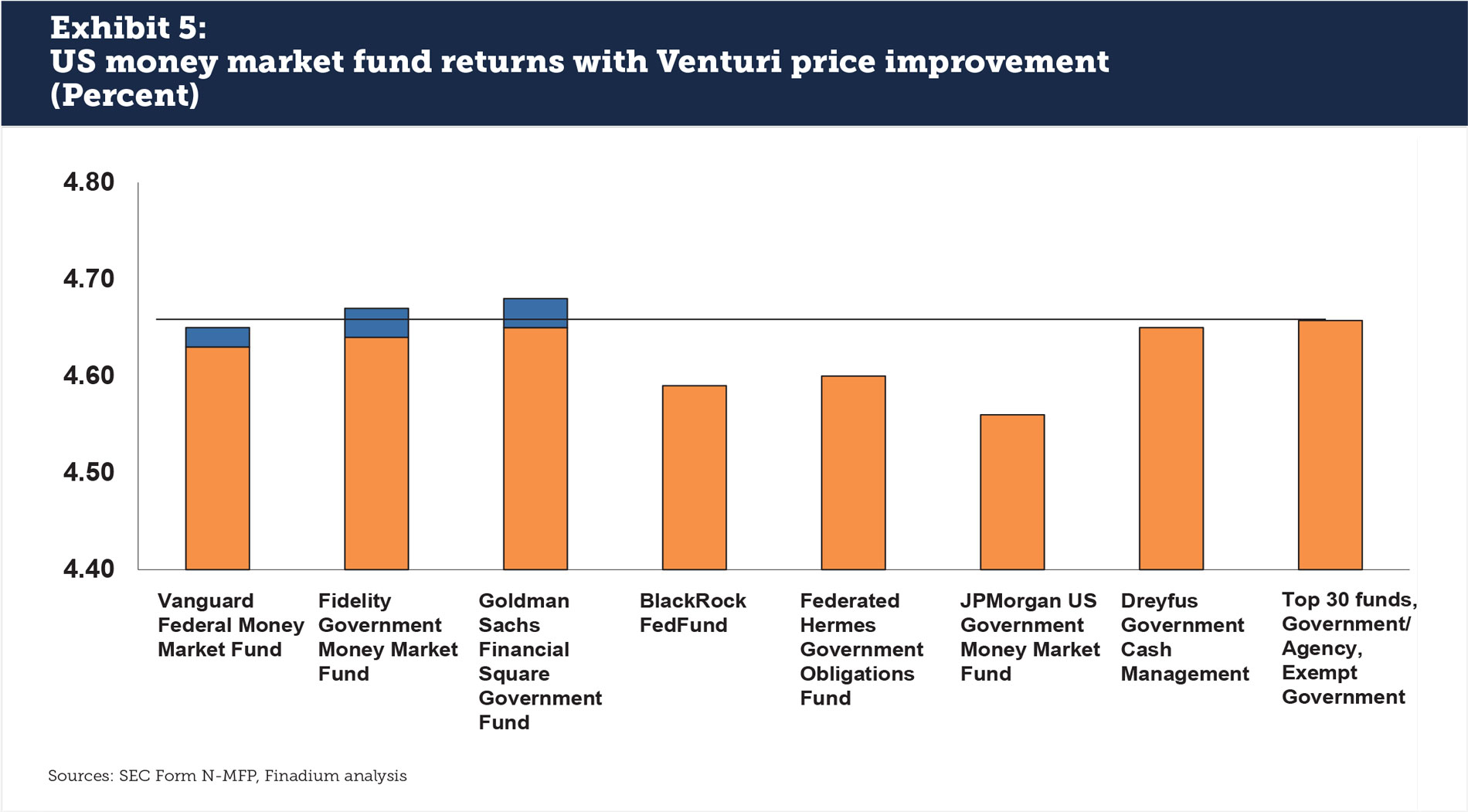

The seven-day yield of the three funds was between 4.63% and 4.65% on February 28, 2023, according to SEC Form N-MFP filings. This was below the average of the top 30 government/agency exempt funds in the market, at 4.66%, but above or about the same as well-known market peers (see Exhibit 4).

We calculated the potential impact of spread improvement on each individual repo position based on collateral type from Form N-MFP, then recalculated what each fund’s seven-day average yield would have been on February 28, 2023. The result was that each fund would have seen a top line return improvement of around three basis points (see Exhibit 5). For the Fidelity and Goldman Sachs funds, this would be enough to beat the average of the top 30 funds in this space. The Vanguard fund would underperform by less than one basis point. Other variations are possible in the calculation, for example removing all non-bank counterparties (applicable to Goldman Sachs only) or making no change when the counterparty is the FICC. Pensions, hedge funds and other investors with a different set of regulatory oversight may see higher returns from engaging in repo with corporate bond or equity collateral; we have observed participation in this strategy from a variety of client types outside the US money market fund space.

Broad access and security from the State Street credit risk guarantee

A fresh look at counterparty default risk is reasonable for any new mechanism in collateralized markets. Even markets that are thought to be well understood can see unexpected changes, including regulatory interventions that cannot be forecasted. The question then becomes whether avoiding these potential uncertainties is worth the loss of price improvement or access to liquidity that lets a money fund beat out a peer benchmark.

The Venturi P2P platform offers investors an opportunity to source liquidity from a wide variety of buy-side participants without the requirement of assessing and monitoring credit risk for each transaction. The State Street guarantee has become the pathway to ensuring protection against credit risk as well as enabling firms without large credit risk oversight divisions an opportunity to engage. This is a new and valuable functionality for the market. While each cash investor will need to make their own assessment on how the guarantee works for their firm, the Venturi platform offers a place to gain a foothold in the broad and increasingly important P2P market.

This article was commissioned by State Street Financing Solutions.