Since the financial crisis regulatory changes and market dynamics have led to an increased usage of non-cash collateral for securities lending transactions. This trend is most dramatic in the U.S., which has historically been a predominantly cash based market. Alternative forms of non-cash collateral such as equities and corporate bonds have seen significant growth as well as borrowers adjust to the new regulatory environment. Lenders that are flexible with permissible collateral will be able to benefit by these market changes. A guest post from State Street.

Non-cash collateral has long been the most prevalent means of collateralizing securities lending transactions (SLTs) in markets outside of the United States. In contrast, the US SLT market has historically relied primarily on cash collateral. The fungibility of cash collateral made it a preference for many borrowers, and the depth of the U.S. money markets provided ample opportunities for securities lenders to return additional low-risk yields to their securities lending earnings. However, the landscape is changing and collateral flexibility is key to maintaining and enhancing securities lending returns.

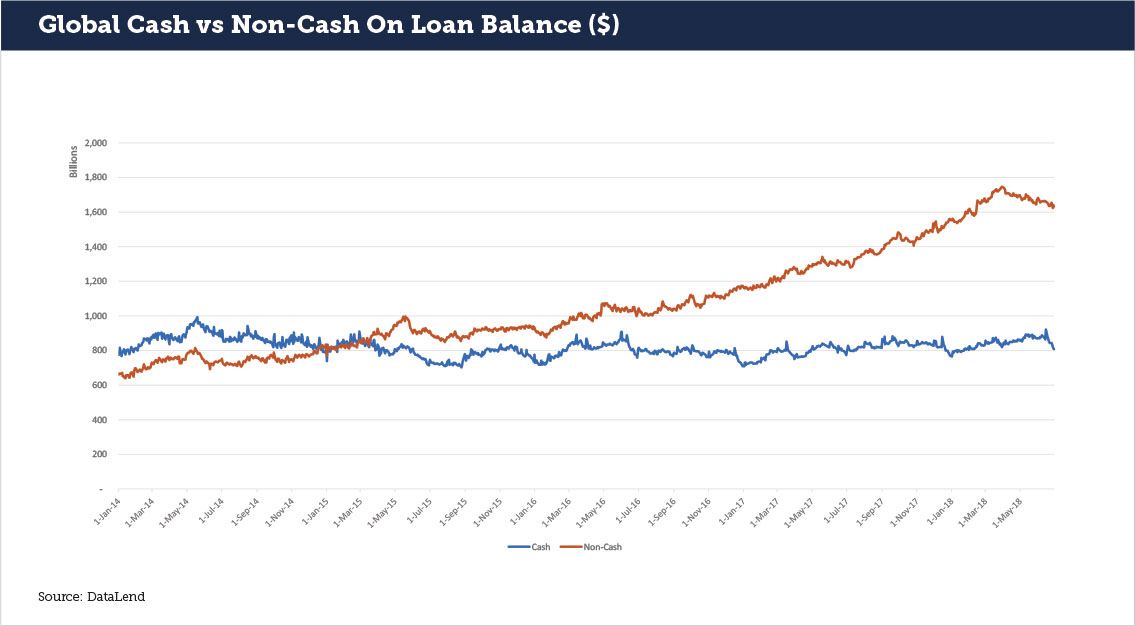

Following the financial crisis of 2008-2009, a number of new regulatory requirements were introduced to ensure banks have sufficient capital and liquidity to withstand a significant market shock. These regulatory changes have driven a significant increase in non-cash collateral usage (and a decline in cash collateral) for SLTs, especially in the US. The regulations largely driving the change in borrower behavior and collateral include the Supplemental Leverage Ratio (SLR), the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ration (NSFR). These changes have dramatically impacted the make-up of collateral within the securities lending market. Since 2014, non-cash balances have more than doubled while cash balances have remained fairly constant.

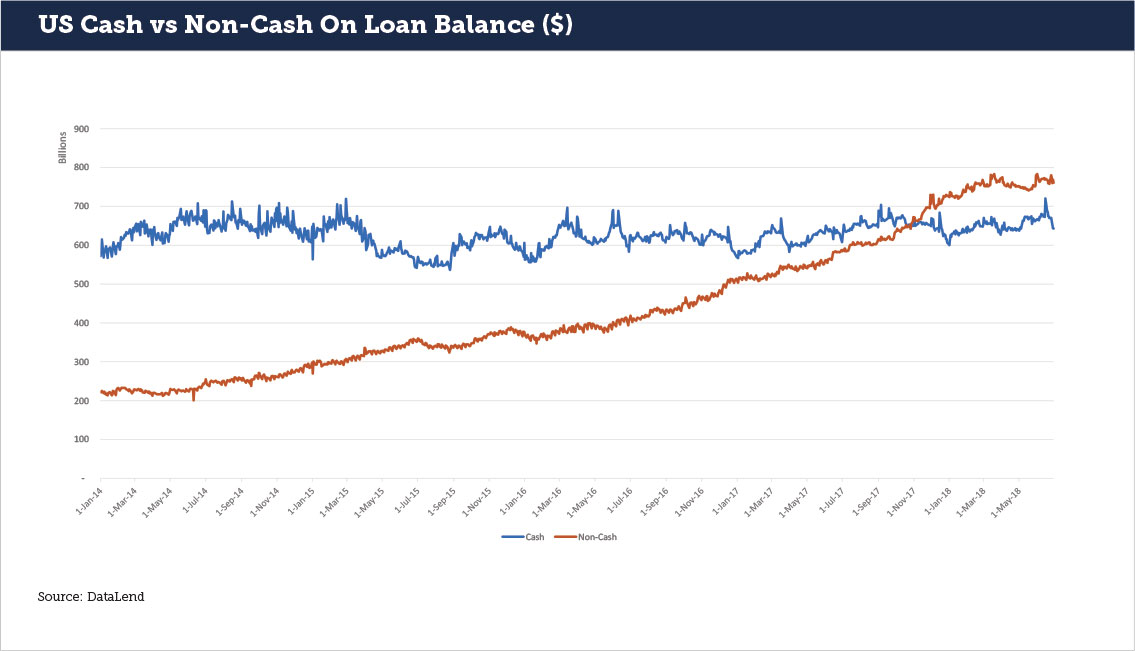

This trend is even more evident in the US market, where non-cash collateral has increased by 4 times while cash collateral has also remained fairly static.

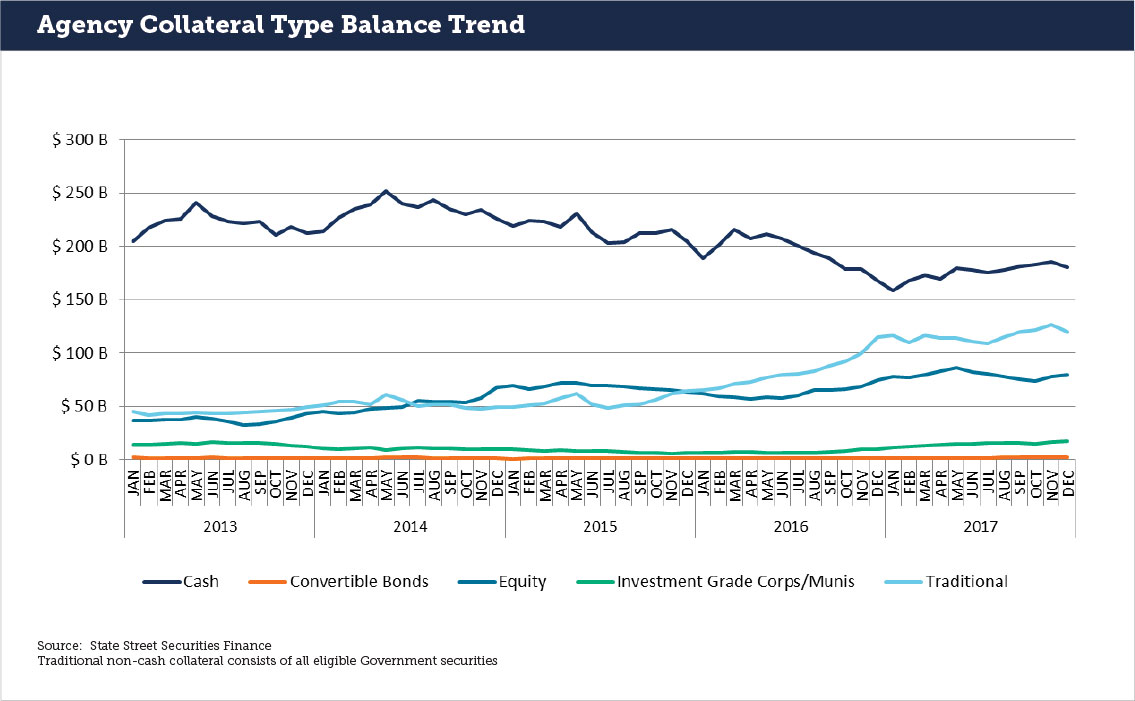

As the following chart indicates, total non-cash loans have increased while loans collateralized by cash have decreased. Both traditional and equity collateral has increased, with smaller growth in corporate bond collateral. The growth in traditional collateral has outpaced equity collateral over the past 2 years as equity collateral growth has been capped to some extent by regulations such as Rule 15(c)3-3 under the Securities Exchange Act in the US, which limits the ability of broker-dealers to pledge equities as collateral in most transactions. Client guidelines which often do not permit equities as collateral have impacted the growth of this collateral source as well.

Regulatory Drivers for Non-Cash Collateral

The Supplementary Leverage Ratio (SLR) increased Globally-Systemically Important Banks sensitivity to balance sheet management. With the increased scrutiny on leverage ratios, banks are taking steps to reduce their balance sheet footprint. Non-cash SLTs can result in reduced balance sheet impacts due to accounting differences between non-cash and cash transactions under U.S. GAAP and the associated rules under Basel III.

The Liquidity Coverage Ratio (LCR) requires that firms measure cash inflows and outflows over a 30 day period based on a prescribed stress scenario with total inflows being capped at 75% of total outflows. Cash based securities loans with a term to maturity of less than 30 days would represent a cash inflow for the borrower; whereas repo transactions with term to maturity of less than 30 days would represent a cash outflow. However, due to the inflow cap of 75% of outflows securities, borrow and repo transactions of less than 30 days are not fully offsetting. The difference between the total inflows and total outflows (net outflows) must be supported with High Quality Liquidity Assets (HQLA) (such as cash and Treasuries and Agencies). However, non-cash collateral does not have a funding component as no cash is exchanged. Thus, the borrower would not have to hold additional HQLA for non-cash loans.

The Net Stable Funding Ratio (NSFR) is yet to be finalized in the United States, but most borrowers have begun to manage their balances sheets to meet the requirements under the current proposal. The NSFR requires banks to maintain appropriate stable funding based on the term to maturity of assets requiring stable funding. Required Stable Funding (RSF) is bucketed into zero to six month, six month to one year, and over one year buckets. Based on the bucket that an asset falls into, the type of transaction and the counterparty type, the bank/borrower will have to maintain a certain percentage of Available Stable Funding (ASF). Bank Liabilities are assigned ASF weights based on the same maturity and other characteristic requirements as the RSF. However, offset trades do not necessarily have the same RSF and ASF percentages. To source this additional funding can be very costly to borrowers; however, if these transactions are done as non-cash transactions there will be no funding component and thus no NSFR impact.

The changing regulatory burdens related to borrowers have substantially increased the cost of borrowing securities against cash collateral. These increased regulatory costs have reduced the return on capital associated with borrowing and on-lending securities against cash. In some instances the regulatory costs have made transactions generate negative real returns. As a result of this dynamic, the market has shifted to an increased preference for non-cash collateral. Historically, non-cash collateral has generally consisted of treasuries, agencies, and sovereign bonds (commonly referred to as traditional collateral) and many regulations and policies require non-cash trades to be collateralized with traditional collateral. However, borrowers are increasingly requesting to pledge equities and corporate debt securities (commonly referred to as alternative collateral). Equities as collateral has grown to be the most common and most desired form of non-cash collateral for borrowers to pledge. This is primarily due to the abundance of equities received as collateral by the borrowers from end users of securities loans, as well as the liquidity profile of main index equities.

Post-financial crisis, the supply of cash investment options has been diminished due to the regulatory changes. The impact of the LCR and NSFR regulations have limited the supply of short term reinvestment options as banks and broker-dealers have looked to lengthen the terms of their funding and utilize evergreen type structures. While some clients have started to utilize such products for a portion of their cash collateral reinvestment, the need for sufficient liquidity to meet daily mark-to-market, return and recall requirements means that a significant portion of the reinvestment portfolios must be in overnight, open or very short term products. In addition, some clients are unable to enter into term repo transactions, thereby limiting their ability to generate sufficient returns. This was exacerbated by money market reform which forced a number of participants to move from Prime Money Market Funds to Government Money Market Funds.

As a result of these regulations, lending performance may be inhibited without increased flexibility. Ultimately the goal of a securities lender and their agent is to optimize the return of their securities lending program within the lender’s risk tolerance level. In order to achieve optimal performance within the set risk tolerance, it is critical to permit all available options that will not cause the program to exceed the risk threshold. For most lenders, from a collateral perspective this means both cash and non-cash should be available options. Additionally, increasing the types of non-cash collateral should be opened to enable the lending agent’s flexibility in adjusting both the risk and return levels.

In addition to increasing flexibility, the market is undergoing changes in trade structures. While Europe has always predominantly been a non-cash market, there is a growing demand to move from a collateral title transfer model to a tri-party collateral pledge structure. The primary driving force behind the demand to shift collateral models in Europe is the potential to significantly reduce RWA utilized by borrowers on non-cash transactions.

Changing Market Structures

Another structural change in the securities lending market is the adoption of Central Counterparties (CCPs). There have been a minimal number of agent lender transactions through CCPs to date. However, many market participants, both borrowers and agent lenders, continue to engage with CCPs to develop a CCP structure that will reduce the regulatory burden on borrowers while maintaining or enhancing the risk return profile for beneficial owners. In addition to developing an appropriate CCP model, there are a number of regulatory changes that will have to be made in order for all lenders to participate in this model.

The changing environment post financial crisis has led to an increased focus on balance sheet and liquidity management with the new regulatory framework. As a result, demand to pledge non-cash collateral, especially alternative forms such as equities, has increased significantly. We anticipate new transaction structures will continue to be introduced. Those lenders that are willing to be flexible in regards to collateral, tenor and trade structure will likely see enhanced utilization and optimal performance going forward.

About the Author

Glenn Horner is a managing director and Chief Regulatory Officer for State Street Global Markets. Mr. Horner advises senior management regarding efficient implementation of regulatory requirements within the division. He works in close coordination with the Bank’s Regulatory, Industry, and Government Affairs unit as well as external industry groups to provide feedback and commentary on regulatory proposals.

Glenn Horner is a managing director and Chief Regulatory Officer for State Street Global Markets. Mr. Horner advises senior management regarding efficient implementation of regulatory requirements within the division. He works in close coordination with the Bank’s Regulatory, Industry, and Government Affairs unit as well as external industry groups to provide feedback and commentary on regulatory proposals.

Mr. Horner joined State Street in 1990. He holds a Bachelor of Science degree as well as a Master of Business Administration degree from Babson College. He also earned the Chartered Financial Analyst (CFA) designation, the Global Association of Risk Professionals’ Financial Risk Management (FRM) certification and the Professional Risk Managers’ International Association’s Certified Risk Manager designation. He is a member of the Association for Investment Management and Research, the Global Association of Risk Professionals, the Boston Security Analysts Society and the Professional Risk Managers’ International Association.

Important Disclosures

This communication is not intended for retail clients, nor for distribution to, and may not be relied upon by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to applicable law or regulation. This publication or any portion hereof may not be reprinted, sold or redistributed without the prior written consent of State Street Bank and Trust Company.

This document is a general marketing communication. It is not intended to suggest or recommend any investment or investment strategy, does not constitute investment research, nor does it purport to be comprehensive or intended to replace the exercise of an investor’s own careful independent review regarding any investment decision.

This document and the information herein does not constitute investment, legal, or tax advice and is not a solicitation to buy or sell securities nor is it intended to constitute a binding contractual arrangement or commitment by State Street of any kind. The information provided does not take into account any particular investment objectives, strategies, investment horizon or tax status. The views expressed herein are the views of State Street Global Markets as of the date specified and are subject to change based on market and other conditions. The information provided herein has been obtained from sources believed to be reliable at the time of publication. The information is complete and accurate to the best of our knowledge. State Street Bank and Trust Company hereby disclaims all liability, whether arising in contract, tort or otherwise, for any losses, liabilities, damages, expenses or costs arising, either direct or consequential, from or in connection with any use of this document and / or the information herein.

This document may contain statements deemed to be forward-looking statements. These statements are based on assumptions, analyses and expectations of State Street Global Markets in light of its experience and perception of historical trends, current conditions, expected future developments and other factors it believes appropriate under the circumstances. All information is subject to change without notice.

Recipients should be aware of the risks of participating in securities lending, which may include counterparty, collateral, investment loss, tax and accounting risks. A securities lending program description and risks statement is available.

Past performance is no guarantee of future results.

This document has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of investment research.

State Street Global Markets is the marketing name and a registered trademark of State Street Corporation, used for its financial markets business and that of its affiliates. Products and services may not be available in all jurisdictions.

The information contained herein is proprietary to EquiLend; may not be copied or distributed without the express consent of EquiLend; shall not constitute investment advice by EquiLend, or any representative thereof; is not warranted to be accurate, complete or timely; is provided for informational purposes only; is not intended for trading purposes; and should not be construed as EquiLend making forecasts, projecting returns or recommending any particular course of action. Neither EquiLend nor any representative thereof shall be an advisor or a fiduciary of a visitor to this website. EquiLend is not responsible or liable in any way to the reader or visitor, or to any person, firm or corporation for any damages or losses arising from any use of the information contained herein. In considering the information contained herein, a reader or visitor to this site does so solely in reliance on the reader or visitor’s own judgment. Past performance is no guarantee of future performance.

© 2018 State Street Corporation