Model risk is a relatively new area that only recently evolved as a separate area from operational risk. The real challenge for model risk is to evolve from a pure cost to a value-added area for financial institutions, writes Maurizio Garro, senior lead for the IBOR Transition program at Lloyds Banking Group.

Garro distinguishes between model validation, which is primarily driven by regulatory requirements, while model risk management is defined as the approach a financial institution uses to assess, mitigate and monitor model risk in line with their risk appetite.

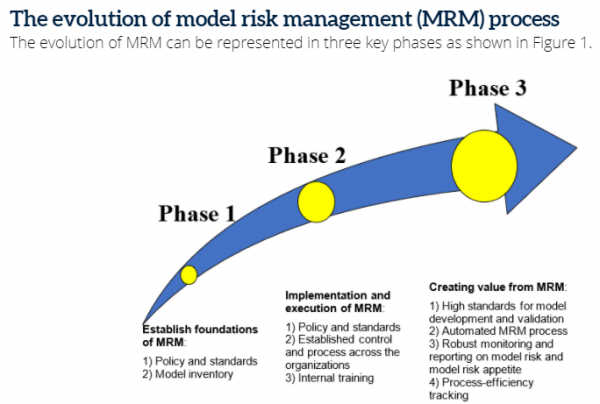

Evolving to value add requires the application of many elements including a consistent model definition and performance monitoring of model risk in line with the risk appetite and business model of the financial institutions. The final step is to identify a coherent and clear way to aggregate and report model risk to allow the senior management to fully understand it in detail, and integrate it into the broader risk management strategy.