The European Central Bank’s recent Quantitative Easing (QE) program is putting a squeeze on European repo markets. QE takes securities out of the market. T2S will help repo by aggregating settlement activity across 22 participating Central Securities Depositories, and hopefully freeing up additional collateral for repo while reducing demand. But is this enough to make a difference in undoing bottlenecks created by monetary policy?

The ECB and Policies for Growth

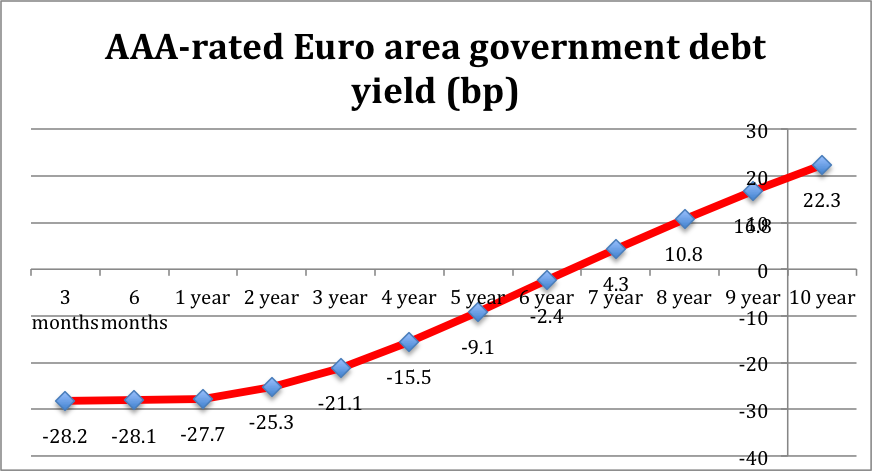

The European Central Bank (ECB) has tried different solutions to fire up the European economy, unfortunately without major success. One tool — negative interest rates — has received a lot of press. The ECB deposit rate is currently -20bp and investors have to go past 6 ½ years to maturity on AAA-rated euro area government bonds to realize a positive yield (1bp). Ten-year bonds earn just 22bp. German bonds had been particularly hard hit.

Source: European Central Bank

The next step was Quantitative Easing, which means the ECB buying upwards of €1.1 trillion of securities at a pace of €60 billion each month. This is not a novel approach for the ECB; in the past they have put in place programs to buy sovereign debt as well as covered bonds. The current ECB balance sheet is about €2 trillion, but the result of QE will be a ballooning figure. In this case, the increase will be in excess of 50%, bringing it back to the 2012 highs caused by the Long-Term Refinancing Operation (LTRO).

The QE program is limited to buying securities that yield better than the ECB deposit rate (currently -20bp) and mature between 2 and 10 years. Also the ECB won’t buy more than 25% of a given issue or 33% of bonds from a given issuer. Given ECB restrictions, a Moody’s report published April 14, 2015 claimed the ECB may very well run out of eligible bonds by the end of 2015. A cut in the deposit rate could give the ECB more flexibility.

Quantitative Easing and the Repo Market

The result of QE has been trouble for the repo market. Liquidity has shrunk as negative rates take their toll and investors hold onto paper. Repo rates on some German government bonds have hit -30bp, below the ECB deposit rate.

The good news is that the ECB has created a facility to lend out paper on repo. This should, on the surface, ease fears of a prolonged collateral squeeze that could cause massive disruptions to the repo market. But looking at the specifics of the program may alter that conclusion. The ECB charges a 40 bp fee to borrow securities for a week. Trades are executed as collateral swaps with a 4% haircut. Borrowers can roll the trade over just 3 times with the fee increasing 10bp each roll. They may not take more than 2.5% of the available amount of any individual issue subject to a hard cap of €200 million per issue. Overall borrower limits will be set by the ECB. Compared to the New York Fed’s program with a maximum cap of US$5 billion maximum, the ECB borrowing programs look shallow for the market.

T2S Can Help Reduce Repo Collateral Shortages

Every step of the way towards freeing up securities needed for collateral will help the repo markets and reduce bottlenecks. T2S consolidates bond market settlement for participating CSDs. This will reduce the need for duplicate CSD settlement accounts and should minimize operational risk. T2S also reduces the web of complexity created by sub-custodians and reduces post-trade costs; this should improve the profitability of securities financing businesses, which in turn may attract new and/or expanded participants to the market.

For broker/dealers or banks facing increased liquidity, leverage and capital constraints, T2S can indeed help by requiring less financing to begin with. Less cash is necessary to keep settlements flowing. Trades will settle in one system, a critical requirement for balance sheet netting under IFRS (and GAAP, as T2S becomes more relevant globally). If more trades can qualify to be netted off the balance sheet, this can provide leverage ratio and capital relief. Tri-party may help by expanding the pool of collateral eligible for a variety of transactions including repo and margin for derivatives.

T2S is a big step forward in fails management, a topic of great importance to the repo community. Through auto-collateralization, T2S will use the value of a security to be settled to collateralize the settlement cash (and vice-versa). For example, instead of having to pre-fund an account with cash to pay for a securities purchase, T2S will effectively fund daylight overdrafts and reduce fails. Minimizing the need to let balances sit idle, auto-collateralization will allow for liquidity to be used more efficiently. Even so, this daylight exposure needs to be managed carefully to avoid the type of unwind/rewind risk absorbed by U.S. tri-party clearers during the financial crisis.

Will T2S specifically ease bottlenecks in the specials markets? Like the rest of repo, the specials market is restrained by capital, leverage and liquidity constraints. But the ECBs quantitative easing program is also hurting the repo markets, perhaps with more immediate and observable impacts. Taking large quantities of securities out of the available float, and imposing high fees to lend them back, saps liquidity in both repo and cash markets. The argument for T2S being a cure is contingent upon more collateral becoming available by virtue of T2S. If T2S settlement aggregation plus tri-party access makes the repo pie larger, it will contribute to greater availability of paper on special.

This article was commissioned by Clearstream.