The reasons why US Treasury fails have increased has been discussed a few times, but a new data analysis from the New York Fed shows more information than we’ve seen previously. Its not just 10 years that have been failing but 30 years and seasoned/lightly seasoned issues too. A key issue is “reopenings,” where the US Treasury issues more of a security that has already been issued. Here are the highlights from the analysis.

(All bullet points citations from the article)

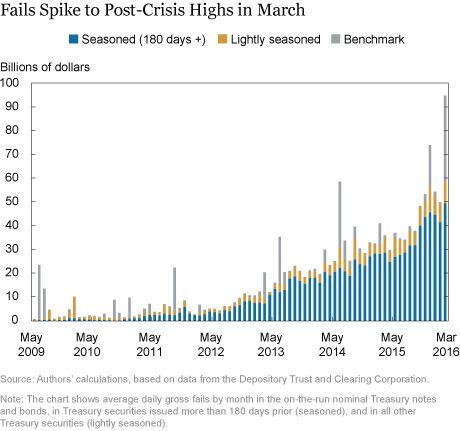

- Settlement fails in U.S. Treasury securities rose to their highest level in more than seven years in March. Among the netting membership of the Depository Trust and Clearing Corporation (DTCC), gross fails (the sum of fails to deliver and fails to receive) aggregated across all Treasury issues averaged $95 billion per day over the month, as shown in the chart below. That said, fails remained well below the historic high of $504 billion per day observed in October 2008 at the peak of the financial crisis.

- Aggregate benchmark fails averaging $36 billion per day and aggregate seasoned fails averaging $50 billion per day. Fails in all other (or “lightly seasoned”) Treasury securities were below post-crisis highs in March, averaging $9 billion per day.

- The trend in seasoned fails seems to have started before recent regulatory initiatives were binding, suggesting that non-regulatory factors are also at play.

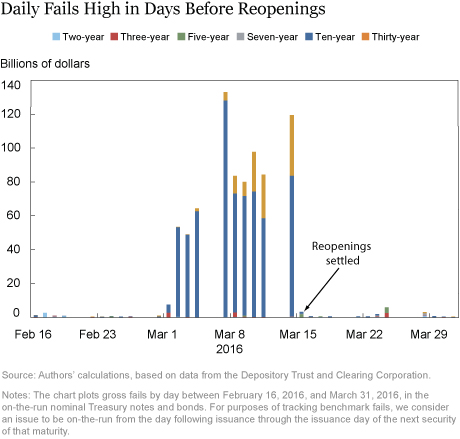

- Interestingly, nearly all of the benchmark fails in March occurred before March 15, as shown in the chart below. The sequential pattern of fails in the days before March 15 is a common feature of benchmark fails because the underlying causes of fails (that is, high demand to borrow securities, low supply of lendable securities, or both) tend to be persistent. On March 15, additional amounts of the outstanding benchmark ten- and thirty-year securities were issued though scheduled “reopenings,” alleviating shortages of those two benchmark issues and quickly clearing the settlement fails in the issues.

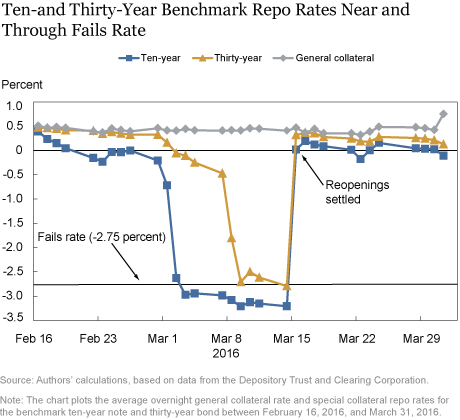

- Market participants reported that the majority of the short base resulted from relative value trading and dealer hedging related to ongoing foreign reserve selling. A range of relative value strategies were at play because the ten-year note was viewed as rich on an outright, curve, and breakeven basis—perhaps making this factor the primary driver of this dislocation.

- It is not unusual for the benchmark ten-year note to become dislocated in the first month after its original issuance.

The full article can be found here: http://libertystreeteconomics.newyorkfed.org/2016/04/whats-behind-the-march-spike-in-treasury-fails.html#.VxTH9z-WZPU