Finadium has updated our data on collateral holdings at CCPs worldwide, but there is a clear lag between CCP reporting on collateral vs. reporting on cleared OTC derivatives by notional values. The results are below.

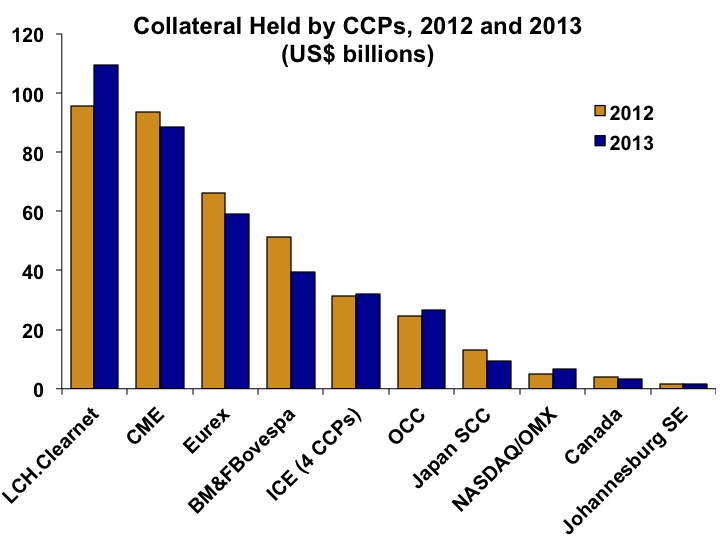

While a few CCPs have collected more collateral than in their previous year’s filings and published data, the overall percentage of collateral held fell by 3%. We found in Q3 2012 that all CCPs we could track held about $400 billion in collateral; our current figures show about $388 billion. NASDAQ OMX, LCH.Clearnet and the OCC showed the biggest collateral gains, while the Japan Securities Clearing Corp and BM&FBovespa showed the most losses.

(Click to enlarge)

For CCPs that saw big changes in collateral holdings, there is a likely correlation there with the amount of business going on. For CCPs with small changes, we think it would be premature to say that a CCP had lost or gained business; collateral holdings could simply be the result of more or less portfolio margining going on.

Here’s the big caveat to these figures: in more recent months since the collateral data above were published, there have been huge changes in CCP notional value cleared activity. A chart last week posted on TheOTCSpace.com showed substantial increases in cleared OTC derivatives business at CME, SwapClear and the Japan Securities Clearing Corp. We expect that the next time collateral figures are released the numbers should shoot upwards at some CCPs.

A lack of current reporting lends credence to a early July argument that CCPs are not providing adequate transparency. An article in the Financial Times on July 7, 2013, said that a group of banks are arguing that CCPs pose a broad risk to the global economy. According to the FT, “Banks have voiced concerns to regulators in Europe and the US that central clearing houses are providing insufficient data on their own risks and demanding lower-quality collateral for swaps transactions. They argue the risks are too opaque, and getting riskier.”

In the end, will estimates (including our own) of CCPs gaining additional collateral holdings of US$1 trillion become a reality? We expect sharply positive changes in collateral holdings at US CCPs in their end of year 2013 reports, following the launch of mandatory clearing of standardized OTC derivatives for Category 1, 2 and 3 clearing firms and end-users. TheOTCSpace chart shows this happening; CCP reports on collateral holdings thus far do not.