The controversy over IM on swap futures versus cleared swaps has made its way into the courts. According to an article in Bloomberg News dated April 16th, Bloomberg LP claimed “…The Commodity Futures Trading Commission, which by law is required to evaluate the costs and benefits of proposed regulations ‘offered only a fleeting, bare-bones discussion of economic effects that contained no financial or quantitative estimates’”.

What is behind this? Bloomberg hopes to operate a Swaps Execution Facility (SEF), as and when the CFTC finishes up writing the rules for SEFs. That process is taking a long time, despite assurances from the CFTC months ago that they are almost done. Cleared swaps, which will go through the SEFs, will compete with swaps futures. Market participants have been debating about the variation between the two and focus on the differences in Initial Margin (IM) models and calculations.

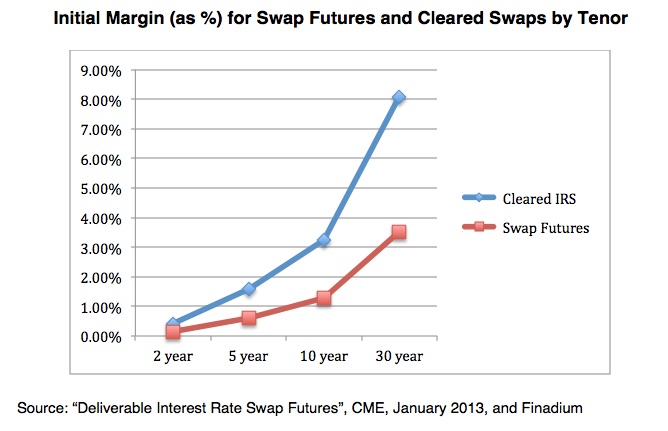

Swap futures use the CME’s SPAN model to determine IM. Cleared futures use some version of VaR. But the driver behind IM is the assumption of how long it will take to liquidate a portfolio in the case of a default. Futures assume 1 day, cleared swaps use 5 days. The futures exchanges historically got to pick which liquidation period they use, cleared swaps are at the mercy of the regulators. (BTW, non-cleared swaps look like they may end up using 10 days according to IOSCO “near final” rules and regs.) The longer the liquidation period, the farther against the FCM the position could go. So a longer liquidation period needs more cushion and hence a bigger amount of IM required. We wrote about this in our recent papers “The Futurization of the Swaps Market: Players, Products and Collateral” (Finadium, March 18, 2013) and “A Guide to Margining for Cleared OTC Swaps vs. Margining for Futures” (Finadium, April 2, 2013). Will less collateral for swap futures siphon business away from cleared swaps (and the SEFs) to the futures exchanges. Bloomberg seems to think so.

This rolls down to collateral management on many levels. The most obvious is less IM >> less collateral >> less demand for eligible paper. Looking at swap futures on the CME versus cleared swaps (also on the CME), the IM differences look like this:

But there are other issues too. Depending on where trades are cleared, they might end up in one cross-margining bucket or another. Clear with the CME and FCMs can look forward to netting futures and swaps. Go with LCH on swaps and until Project Trinity, which is slated to net FICC cash & repos, LCH swaps, and LIFFE futures is up and running, there is no cross market netting. Netting LCH cleared swaps against CME swap futures is not likely. While everyone does the optimization game in picking where they clear what product, individual CCP and DCO market share may come under threat. This is not lost on those pulling the strings behind the various mergers of exchanges and clearinghouses (LCH and LSE, ICE and NYSE Euronext).

On a FCM client level, cross netting across clearing platforms is available (although we have heard differing opinions on well it works). But while trades net down at the investors FCM account, decomposed margin may create the need for the FCM to post more than they ask from their client. This results in an extension of credit that, while it may be profitable, may not be the FCMs first choice of how they want to operate.

So how does this come back around to Bloomberg and SEFs? One major dimension of the decision to go with a swap future or a cleared future is IM. We suspect that SEFs see the 5 day liquidation period as “carved in stone”. Their likely objective is to push the swap futures market away from their traditional 1 day liquidation to a 5 day time horizon. The CFTC has been skeptical of the OTC market participants arguments, relying on the future’s industry “it didn’t break in the financial crisis, don’t fix it” approach. Pushing the decision into the Courts will pressure the CFTC.

A link to the Bloomberg article is here.

A link to a synopsis of “The Futurization of the Swaps Market: Players, Products and Collateral“ is here.

A link to a synopsis of “A Guide to Margining for Cleared OTC Swaps vs. Margining for Futures” is here.