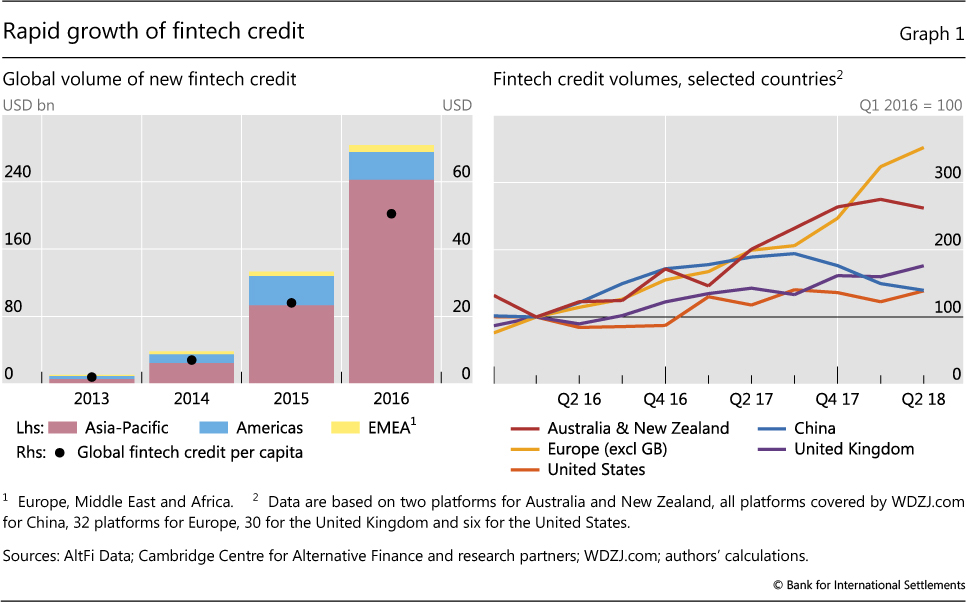

Fintech credit has grown rapidly since its inception in 2005. Fintech credit volumes per capita appear to reflect a number of factors. The economy’s overall development, the competitiveness of the economy’s formal banking sector, and the strength of its regulatory environment play important roles. Despite its fast expansion, fintech credit remains relatively small in most economies. It is, however, considerably larger in China, the United States and the United Kingdom, as well as in specific market segments.

Fintech credit has in some cases helped improve credit access for financially underserved firms and individuals, while providing additional options to investors. Yet rising credit losses in some jurisdictions suggest that these innovations need to be further tested over a full financial and economic cycle. The diversity of business models across the industry has given rise to significant challenges for practitioners and policymakers alike. These challenges include ensuring adequate consumer and investor protection, and the timely assessment of overall financial stability and economy-wide risks. The challenges and benefits arising from fintech credit may become greater if commercial banks make more extensive use of these innovations.