The latest post on the FRB-NY’s Liberty Street Economics blog is “Lifting the Veil on the U.S. Bilateral Repo Market”. Written by Adam Copeland, Isaac Davis, Eric LeSueur, and Antoine Martin, it addresses some important issues on sizing and composition of the repo market. It is worth a look.

The article differentiates between the information available on the bilateral repo market and tri-party. We know that tri-party has fairly good data available, found in the Tri-party Repo Statistical Data published monthly. The Fed breaks down by asset class (including top 3 dealer concentration levels) and haircuts. In addition, data on General Collateral Finance (GCF) Repo is available. GCF is settled through tri-party.

Bilateral trades are another world altogether. Data is pieced together, filled with lots of assumptions. From the post “…While there are public data about the tri-party repo segment, there is little to no information on the bilateral repo segment…” We agree and have written about the lack of good data on bilateral repos in a Sec Fin Monitor post on June 12th “The Fed updates the Flow of Funds data revealing a better picture of the repo market” and a Finadium report “The US Repo Market in 2014”.

The authors have a methodology they are refining to get to a reasonable estimate of the bilateral market.

“…Primary dealers provide information about their total repo activity by type of collateral, but this information does not distinguish between the bilateral and tri-party repo segments. We also have data on the collateral posted in tri-party repo. For each asset class we consider, we can deduct the activity in the tri-party repo (including the gross amounts traded in GCF Repo®) from the activity in the overall repo figure reported by primary dealers to obtain an estimate of the amount of collateral financed in the bilateral repo segment…”

The underlying data from the Primary Dealers comes from “Government Securities Dealers Reports” FR 2004. Tri-party data includes numbers from all dealers, but the FR 2004 only includes primary dealers. The authors make an adjustment for this, assuming that primary dealers account for 80% of the bilateral market. They also adjust for differences in haircuts. Still, there are other definitional differences that are hard to adjust for.

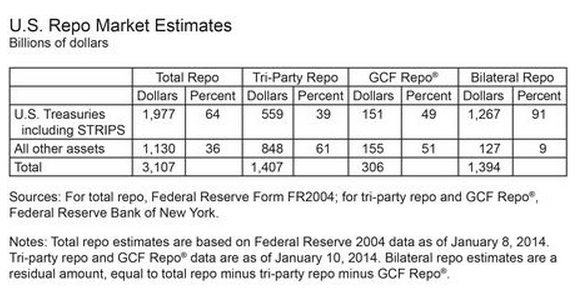

The breakdown for the market looks like this:

There was some surprise at the collateral mix in bilateral repo.

“…The striking fact is that Treasury securities make up 90 percent of the collateral posted in bilateral repo. Other securities, such as agency mortgage-backed securities (MBS), agency debt, corporate bonds, and equities, are posted as collateral in bilateral repo trades, but only to a limited extent. In contrast to bilateral repo, Treasury securities play a much smaller role in tri-party repo. Treasury securities are posted as collateral for roughly 40 percent of tri-party repo trades, about the same share as agency MBS…”

We aren’t very surprised by this. Bilateral trades are about covering shorts. You can’t do this in tri-party (at least, not easily). Shorts in non-Treasury paper are much less common. Tri-party is driven by funding trades on general collateral – the stuff that has no scarcity value. The attractions of tri-party (including settlement ease and lower transactional costs) are compelling. While both bilateral and tri-party trades share basic characteristics – cash goes one way, bonds the other and then back again at maturity – they really are two different animals. The Fed even says as much:

“…The dominant use of Treasury securities as collateral in bilateral repos is reportedly driven in part by demand for specific Treasury securities. Tri-party repo is not conducive to these collateral-driven trades because tri-party repos are designed to be general collateral trades, which means that the institution delivering cash agrees to accept securities within a broad collateral class (for example, investment grade bonds, or U.S. Treasury securities with maturities less than ten years). As such, if a financial institution is looking for a particular piece of collateral, such as an on-the-run Treasury security, then bilateral repos are the more appropriate way to obtain that security compared to tri-party repo…”

But there are a lot more questions than answers. The post asks:

“…Of particular interest is the amount of bilateral repo that is interdealer, the extent to which bilateral repo trades reflect activity driven by demand for specific securities, and the velocity of securities among dealers within a day. Among the data that would help us better understand the U.S. repo market are the level of haircuts, the size, the interest rate, the counterparty, and the tenor of trades. Some of these data are available for the tri-party repo market, but not for the bilateral market. So while we are able to shine a little bit more light on the U.S. repo market, we continue to need more data to further our understanding of this critical market…”

The opacity of the bilateral repo market needs to break down. We think it is a shame that there is no equivalent to the ICMA repo market surveys. The SIFMA Funding Executive Committee might be a good place to take this work on, but it doesn’t feel like it has been a priority. There is a lot of misinformation out there about the repo markets. A little sunlight might do a world of good.